After gradually withdrawing capital from China and making a lightning investment in Taiwan, billionaire Warren Buffett is now focusing on the "big 5" of Japan.

As of the end of March, Berkshire Hathaway's portfolio was worth $328 billion, with 77% made up of five US stocks: Apple, Bank of America, American Express, Coca-Cola and Chevron.

However, in recent years, billionaire Warren Buffett has increased his investment in Asia. He started with an investment in PetroChina in 2002, then in South Korean steelmaker Posco in 2006, holding it for about a decade.

In 2008, he invested in Shenzhen-based electric carmaker BYD. Asia now accounts for much of the growth in Berkshire’s portfolio, and its moves there are increasingly of interest to investors.

Take Berkshire Hathaway’s short-lived relationship with TSMC. Known as a long-term investor, in what investors consider an “unusual” move, Berkshire Hathaway bought $4.1 billion worth of TSMC shares in 2022 and sold them just a few months later. In its latest quarterly report in May, Berkshire no longer held any shares in the Taiwanese semiconductor company.

According to Nikkei , this decision shows that Berkshire Hathaway is not concerned about geopolitical risks and that he is not comfortable after buying TSMC shares. At the recent shareholder meeting, Buffett said he had reassessed. Previously, in April, during a trip to Japan, billionaire Buffett hinted that geopolitics was "certainly worth considering".

In return, Berkshire Hathaway’s money has flowed more to Japan. Last month, billionaire Buffett announced that he had increased his stakes in five of the country’s oldest conglomerates by 7.4%. They are Itochu, Marubeni, Mitsubishi, Mitsui & Co, and Sumitomo. Berkshire’s total market capitalization of Japanese companies as of May 19 was about 2.1 trillion yen ($15.2 billion), making the group the largest investment outside the United States.

“I feel better about the capital I have deployed in Japan than I do in Taiwan,” Buffett told shareholders. Aside from geopolitical reasons, which he doesn’t often mention directly, the decision to move capital from China and Taiwan to Japan was a simple economic decision for him.

Japanese companies have a track record of stable earnings, decent dividends and consistent stock buybacks — something Buffett has repeatedly advocated, arguing that buybacks increase ownership in a company without actually buying more of it.

Moreover, all five Japanese conglomerates were trading below book value, with dividend yields of around 5%, when Buffett invested in 2019. “They were selling at prices that I felt were absurd, especially relative to prevailing interest rates at the time,” he commented.

The five companies’ latest annual results, released on May 9, showed strong gains in profits and dividends. In the fiscal year ended March, the five companies’ combined net profit was 4.2 trillion yen, up 19 percent from a year earlier. Their combined cash dividend payments were 957 billion yen, up 20 percent.

Assuming Berkshire buys 7.4% of the companies before the ex-dividend date, the dividend income would be about $510 million. Under the dividend payment plan for the five companies, that figure is expected to rise to $565 million for the fiscal year ending March 2024. That’s not insignificant compared to the $704 million Berkshire received from Coca-Cola last year.

Why did Warren Buffett choose Japan as the place to invest the most? Part of the appeal of Japanese companies, Buffett says, is that they have many similarities with Berkshire Hathaway. Like Japanese conglomerates, Berkshire Hathaway is a holding company with many assets.

Specifically, Berkshire is a conglomerate with six operating segments, including insurance, railroads, utilities and energy, manufacturing, wholesale grocery distribution, services and retail. It owns and operates real businesses, such as the Geico auto insurance company, See's Candies and Burlington Northern Santa Fe (BNSF), one of the largest railroads in North America.

The original Japanese term for the five companies he invested in is “sogo shosha,” which literally means “comprehensive trading company.” The five companies have similar businesses to Berkshire and have a long history, most of which date back to the Meiji Restoration. Mitsui and Sumitomo even date back to the 17th century.

Investing in Japan also allows Berkshire to take advantage of extremely cheap financing. It has raised Japanese cash through a series of local bonds over the past five years, earning interest rates significantly lower than those in the United States. “It’s working out very well,” Buffett told shareholders at a recent meeting. He plans to increase his stake to 9.9% of each company and is considering potential partnerships. “We’ll continue to look for more opportunities,” he added.

Buffett’s business trips outside the United States are extremely rare. Although Japan is the largest Asian investor, his visit last month was only his second since November 2011. Kenichi Hori, Mitsui’s chairman and CEO, described the meeting with Buffett in Tokyo as “productive,” as he felt Berkshire’s management understood its business model.

Berkshire’s commitment to Japan has also boosted the country’s stock market. The Nikkei 225 has risen nearly 40% since Buffett disclosed his investments in five Japanese companies in late August 2020. It is approaching its all-time high, reached in December 1989.

Toby Rodes, co-founder of Kaname Capital, a US investment fund, said the Japanese stock market is much cheaper than when it last hit a record high. "That's why Warren Buffett and a lot of people are attracted to this market, because they see real value," he explained.

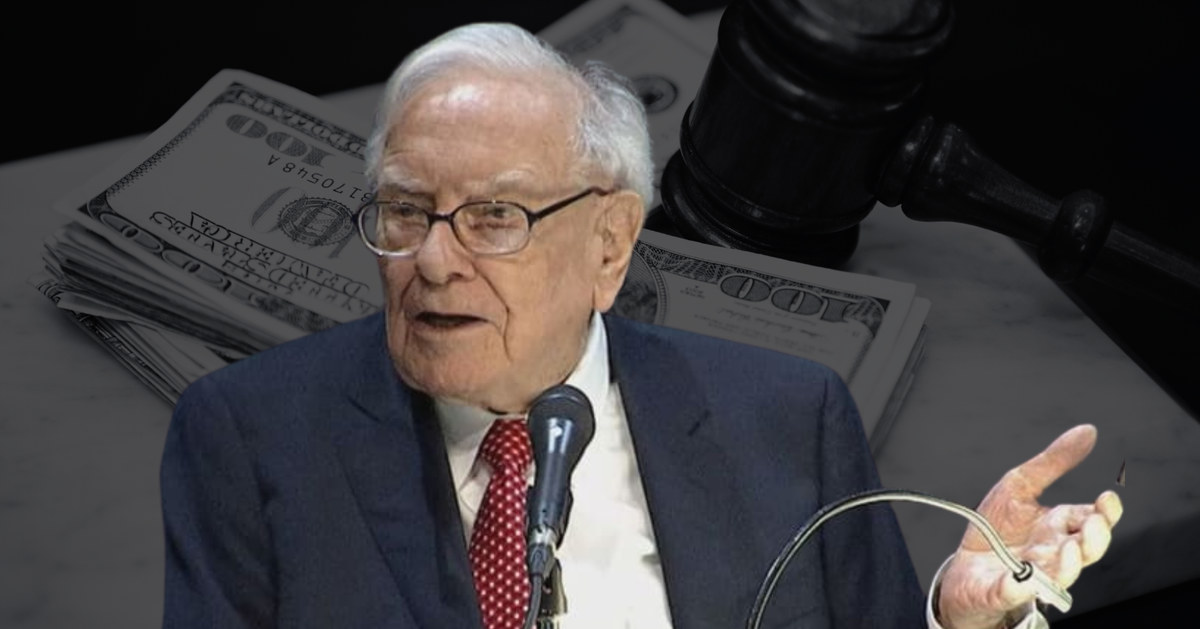

Billionaire Warren Buffett. Photo: Nikkei

But according to analysts, Buffett's strategy of investing heavily in five Japanese companies has other benefits behind it. That is an indirect way to access opportunities in the Chinese market as Berkshire gradually withdraws direct investments.

All five Japanese companies have varying degrees of exposure to China. Their various natural resource-related businesses are heavily dependent on Chinese demand. They also have direct investments in the country.

Itochu’s former chairman was Japan’s ambassador to China. The company holds three-way capital and strategic alliances with Chinese state-owned conglomerate Citic and Charoen Pokphand, a Thai conglomerate with close ties to China for nearly a decade.

Richard Kaye, portfolio advisor and analyst at Comgest Asset Management Japan, said another reason Berkshire chose to invest in the five Japanese companies is so they can act as a “proxy” for Berkshire to access the growth of the world’s second-largest economy, given the close business connections and interactions between Japan and China. “Japan is the best platform in the world to invest in China’s growth,” Kaye noted.

Meanwhile, Buffett has been pulling back on his direct investments in China that he began in 2002-2003. Most notably, his $488 million stake in PetroChina. At the time, the PetroChina purchase was a surprise given Buffett’s longstanding investment philosophy of being a U.S.-only player.

But Berkshire came under fire for its investment in PetroChina as violence in Darfur, Sudan, intensified in 2007. PetroChina's parent company, China National Petroleum Corporation (CNPC), owns a significant stake in the local oil company there.

In February 2008, Berkshire announced that it had sold all of its PetroChina shares the previous year. Buffett cited the dramatic rise in oil prices and the subsequent rise in the stock price, not mentioning the Darfur crisis.

PetroChina's share price peaked at HK$20.25 in November 2008 after Berkshire's sell-off and has not reached that level since. It closed at HK$5.40 on May 19. Although it became a public relations nightmare, Buffett's attempt to "exit" the position was "a resounding success," according to Nikkei .

Berkshire’s latest big bet on China is BYD, the electric-vehicle maker Buffett first invested in 15 years ago. The company is poised to become China’s best-selling car brand, on track to surpass Volkswagen this year.

By early May, Berkshire had 108.34 million BYD shares, or about 3.7%, including the Shenzhen-listed shares, down from about 225 million shares it initially bought in September 2008.

Since the initial purchase price was HK$8 per share while the selling price was around HK$200 or more per sale, Berkshire is estimated to have earned more than HK$6 billion ($765 million) in cash and more than HK$5 billion in profits so far.

Berkshire executives have not said why they are gradually withdrawing from BYD. Some speculations include doubts about the future of the auto industry and geopolitical considerations. “The auto industry is tough,” Buffett said. He said it is an industry with many competitors around the world and acknowledged that it is impossible to predict what will happen in the next five to 10 years.

Additionally, concerns such as Ant’s canceled IPO in November 2020 and the subsequent disappearance of Alibaba founder Jack Ma have significantly changed Buffett’s view of China. Jack Ma has since resurfaced, but the incident is a reminder of the risks of investing directly in Chinese companies.

A Hong Kong-based hedge fund manager who spoke on condition of anonymity said it was understandable that Berkshire saw risks associated with dealing directly with China, especially as an American company.

Warren Buffett and Berkshire Vice Chairman Charlie Munger do not want tensions between the US and China to escalate further. At the Omaha AGM, Munger stressed that both sides are making the situation precarious. He believes that the US and China are “equally at fault” for the ongoing consequences.

Citing the case of Apple, where Berkshire is heavily invested, Munger said that working with China has paid off and that it is “good for Apple and good for China.” Buffett compared the current arms race between the two superpowers to the nuclear arms buildup during the Cold War. The investor believes that what the US now faces with China is a “different game,” with “more destructive tools” at both sides’ disposal, including cyberwarfare.

“It is imperative that both China and the United States understand that we cannot push each other too hard,” Buffett said. “We will be more competitive, but we should assess how far the other side will not react,” he added. And at Berkshire, Buffett seems to be playing the long game in this new situation. “We are just getting started in this game,” he said.

Phien An ( according to Nikkei )

Source link

![[Photo] Paris "enchanted" by the blooming flower season](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/3/21/e967dc548ff74f9ca8e89d72c3608825)

![[Photo] President Luong Cuong receives former Vietnam-Japan Special Ambassador Sugi Ryotaro](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/3/20/db2d8cac29b64f5d8d2d0931c1e65ee9)

Comment (0)