From the beginning of the year to the end of last week (June 7), the performance of banking stocks showed differentiation, with many stocks increasing very strongly, but some stocks also increased lower than the VN-Index.

Banks, the largest group of stocks in terms of capitalization on the stock exchange, accounting for over 30% - have a big impact on the VN-Index, showed a good leading role in the first quarter of the year (thanks to a positive business picture in the fourth quarter of 2023), then had a quiet performance because the first quarter of 2024 numbers were not as expected.

|

| Bad debt ratio of listed banks |

Mr. Dang Van Cuong, Head of Brokerage Department of Mirae Asset Securities Company, said that according to statistics, the bad debt ratio of 27 listed commercial banks has increased from 1.96% in the fourth quarter of 2023 to 2.18% in the first quarter of 2024, although the lending interest rate level is still at a historical low. The main reason is the decline in debt repayment capacity of individuals and businesses due to income difficulties, low new orders and reduced liquidity in the real estate market, combined with slow credit growth.

With rising bad debt, the industry's bad debt coverage ratio decreased from 106% in the same period to 86.87% in the first quarter of 2024.

|

The banking system's NIM has been on a continuous downward trend in recent quarters, with the first quarter of 2024 falling to 3.4% from 3.73% in the same period. The current downward trend in NIM is mainly due to limited credit growth and banks having to cut interest rates to support customers, as they are facing many difficulties in cash flow. Capital costs tend to decrease, but interest income also decreased rapidly in the last quarter. According to Mr. Cuong, all banks' NIM has decreased compared to the same period, but compared to the fourth quarter of 2023, there are banks with improved NIM including CTG, VCB, TCB, HDB, LPB, TPB.

|

| NIM of banks |

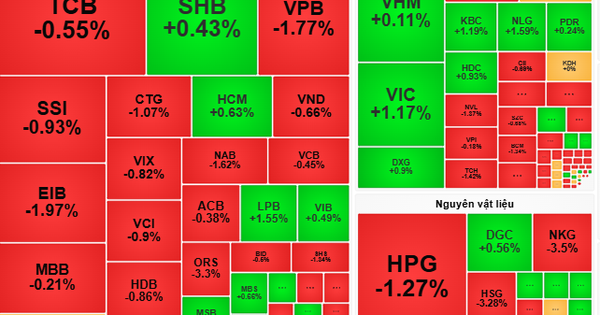

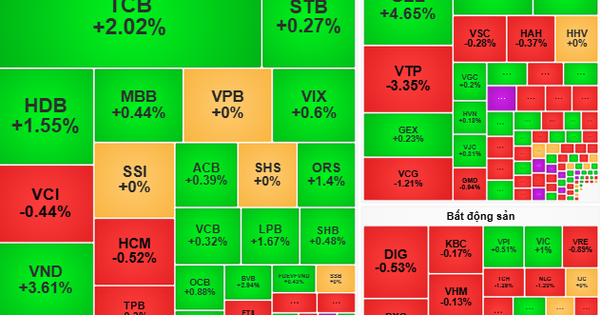

Returning to the stock prices of the banking group, from the beginning of the year to the end of last week (June 7), many stocks had strong and impressive increases such as LPB increased by 66%, TCB increased by 59.2%, MBB increased by 23%, ACB increased by 22.5%, VIB increased by 21.1%, CTG increased by 21%, while stocks VCB, STB, BID, SHB... had an increase of less than 10%, lower than the performance that VN-index achieved.

Recently, in the pillar group, there have been strong increases such as banking stocks as well as information interest from investors, such as STB, CTG, TCB, MSB, VIB, MBB...

Mr. Cuong said that there are some positive signals for this group. Credit growth by the end of May increased by 2.41% compared to the end of 2023 (equivalent to an increase of 12.8% over the same period). Credit growth is growing very well after a period of slow growth (by the end of the first quarter, it only increased by 0.26% compared to the beginning of the year). Thus, from the beginning of the year to the end of May, outstanding credit has increased by more than VND 326,800 billion, which has been put into the economy, a sign that the ability to absorb capital as well as the demand for loans is improving.

Mr. Cuong said, recorded information showing that credit growth of some banks by the end of May such as LPB increased by 10.6%, TCB increased by 9.9%, ACB increased by 6.7%, CTG increased by 4%, STB increased by 3.7%, BID increased by 2.3%, MBB increased by 1.8%; two large state-owned banks VCB increased by negative 0.4% and Agribank increased by negative 0.2%.

Net interest income is a key source of revenue in the operating model of banks, so the very good credit growth at LPB and TCB as well as the positive business results in the first quarter, according to Mr. Cuong, are important reasons explaining the outstanding price increase of these two stocks. The upcoming prospects of the banking industry will be clearer thanks to factors including:

(1) Faster credit growth and a slight decline in the bad debt ratio as the financial and business fundamentals and customer demand (enterprises and individuals) recover. Businesses continue to receive many new orders and the real estate market warms up with increased liquidity is the expected scenario.

(2) NIM will improve from Q3/2024 as lending rates edge up at a higher rate than deposit rates and personal lending at banks grows more strongly in the second half of the year.

|

|

| Valuation of some listed banks based on current P/E and P/B ratios |

Divergence in business results and financial status of banks will continue in the coming quarters. In terms of investment opportunities, investors should carefully analyze and invest in bank stocks with higher credit growth rates than the industry average and good risk management capabilities at low valuations compared to history.

In addition, stories related to completing restructuring projects to enter a new growth cycle, paying cash dividends or issuing shares to increase charter capital are also worth paying attention to in some banks, Mr. Cuong said.

Source: https://baodautu.vn/co-phieu-ngan-hang-phan-hoa-va-co-hoi-d217435.html

![[Photo] Vietnamese rescue team shares the loss with people in Myanmar earthquake area](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/6/ae4b9ffa12e14861b77db38293ba1c1d)

![[Photo] Solemn Hung King's Death Anniversary in France](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/6/786a6458bc274de5abe24c2ea3587979)

Comment (0)