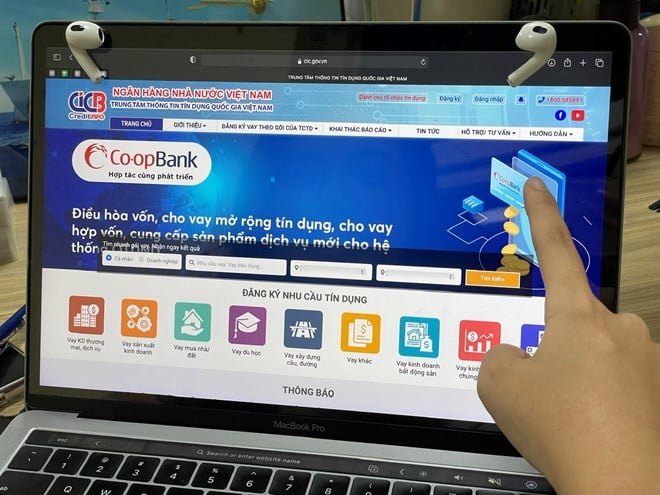

What is credit information?

Credit information is information about borrowers and information related to borrowers at credit institutions and foreign bank branches. In Vietnam, the credit information activities of the State Bank of Vietnam (SBV) are regulated in Circular 03/2013/TT-NHNN dated January 28, 2013, specifically on the rights and responsibilities of relevant organizations, including the National Credit Information Center of Vietnam (CIC), a unit under the SBV, which is the focal point for credit information activities of the SBV.

CIC is a public service organization that performs the function of collecting, processing, storing, and analyzing credit information; serving the State management requirements of the State Bank; providing credit information products and services according to the regulations of the State Bank and the law.

Currently, the Vietnam National Credit Information Database managed by CIC stores information of more than 54 million borrowers, with the participation of 100% of credit institutions operating in Vietnam and voluntary organizations reporting information.

What is a credit score?

A credit score is an indicator of a borrower's creditworthiness. The score indicates the likelihood that a borrower will repay their debts and pay their bills regularly and in full. A higher credit score corresponds to a lower risk of default and a higher likelihood of obtaining credit.

Each agency or organization that conducts credit scoring will have scales corresponding to different levels of risk. At the National Credit Information Center of Vietnam, credit scores are the result of a calculation process that combines credit information of borrowers, including identification information, information about customer debt balances, and some other related information.

According to the CIC's individual credit scoring model, the credit score of the borrower is applied according to the principle that a high score corresponds to a high level of creditworthiness, so the possibility of future risks is low; and vice versa, a low credit score means a high possibility of future risks. The credit score of the borrower (from 403 to 706) is divided into 5 levels: Bad, below average, average, good and very good corresponding to decreasing levels of risk.

Improve credit score, avoid bad debt

To maintain and improve credit scores, each individual should consciously control their credit usage behavior and properly fulfill their debt repayment responsibilities to lending institutions. CIC provides some criteria and guidelines for customers to refer to in order to improve their credit scores and access credit more easily at credit institutions as follows:

- Only borrow money/open a credit card when really necessary and carefully calculate your ability to repay based on your actual income.

- Have a plan to repay debt in full and on time: Always consider your financial ability to plan your spending to repay debt in full and on time; always be conscious of repaying debt, even if it is a small debt (you can use automatic debt reminder tools such as phone reminder software).

- Regularly check your credit information to monitor your information and creditworthiness and avoid being taken advantage of by scammers. Have a plan to handle it if you find that your information is inaccurate.

- When having many debts at the same time, customers should try to gradually pay off the current debt balance, should not incur many new debts, especially unsecured debt and consumer loans.

Source

![[Photo] Prime Minister Pham Minh Chinh and Brazilian President Luiz Inácio Lula da Silva attend the Vietnam-Brazil Economic Forum](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/3/29/f3fd11b0421949878011a8f5da318635)

![[Photo] Prime Minister Pham Minh Chinh chairs meeting to urge highway projects](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/3/29/6a3e175f69ea45f8bfc3c272cde3e27a)

![[Photo] Dong Ho Paintings - Old Styles Tell Modern Stories](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/3/29/317613ad8519462488572377727dda93)

Comment (0)