The central exchange rate decreased by 2 VND, the VN-Index stood at 1,275.14 points or the estimated disbursement of public investment capital in the 12 months of 2024 only reached over 77.55% of the plan... are some notable economic information in the week from December 23-27.

| Economic news review on December 25 Economic news review on December 26 |

|

| Economic news review |

Overview

Estimated disbursement of public investment capital in the first 12 months of 2024 only reached over 77.55% of the plan, the target of achieving a disbursement rate of 95% of the public investment capital plan in 2024 is difficult.

According to the Ministry of Finance's report, by the end of November 2024, the country's public investment disbursement reached 52.72% of the plan and 58.2% of the plan assigned by the Prime Minister. It is estimated that by the end of December 2024, the country will have disbursed over VND 529,632 billion, reaching 77.55% of the plan assigned by the Prime Minister.

Thus, the estimated 12-month disbursement rate of the whole country is lower than the same period in 2023 (in 2023, the disbursement rate of the whole country reached 73.5% of the plan and 81.87% of the plan assigned by the Prime Minister). Of which, the estimated 12-month disbursement of central budget capital reached over 72%, higher than the same period in 2023 (nearly 70%), but the estimated 12-month disbursement of local budget capital reached over 69% of the plan and over 80% of the plan assigned by the Prime Minister, lower than the same period in 2023 (in 2023, the rates were 76% and 94%, respectively).

Regarding the disbursement of planned capital from previous years extending to 2024, the report from the Ministry of Finance said that the cumulative disbursement from the beginning of the year to the end of November 2024 was VND 23,864.6 billion, reaching 41.65% of the plan. The estimated disbursement from the beginning of the year to December 31, 2024 was VND 38,605.2 billion, reaching 67.38% of the plan.

The report from the Ministry of Finance also said that the capital under the Economic Recovery and Development Program had a high 12-month disbursement rate of 91.75%. Of which, the capital of the Recovery Program managed by ministries and central agencies reached 99.8% (the Ministry of Public Security and the Ministry of Transport alone reached 100%).

As the above figures show, achieving the target of 95% disbursement of the 2024 public investment plan is quite difficult. According to the Ministry of Finance, with just over a month left until the end of the 2024 public investment period, there are still 30 ministries, branches and 26 localities with estimated disbursement rates lower than the national average. Notably, Ho Chi Minh City - one of the two major economic locomotives of the country - was assigned a very large 2024 public investment plan of over VND 79,263 billion, accounting for 11.8% of the plan assigned by the Prime Minister to the whole country, but so far only over 51% has been disbursed, which has greatly affected the overall disbursement rate of the whole country.

The Ministry of Finance said that the Government has submitted to the National Assembly for promulgation a number of laws (such as: Law amending 9 laws related to the field of budgetary finance, Law amending Public Investment; Law amending and supplementing a number of articles of the Law on Planning, Law on Investment, Law on Investment under the form of public-private partnership, Law on Bidding) to create a transparent mechanism in the management of public investment projects. However, these laws are expected to take effect from 2025.

Therefore, the problems in disbursing public investment capital in 2024 have not been completely resolved. In addition, in reality, there are still some inherent difficulties affecting the progress of disbursement of projects that have not been completely resolved, such as: problems in site clearance, land use planning and supply of raw materials; problems in completing investment procedures, disbursement processes of ODA projects... which need to be actively and proactively resolved by ministries, branches, localities and investors to speed up the progress of disbursement of public investment capital.

Domestic market summary week from December 23-27

In the foreign exchange market during the week of December 23-27, the central exchange rate was adjusted up and down alternately by the State Bank. At the end of December 27, the central exchange rate was listed at 24,322 VND/USD, down only 2 VND compared to the previous weekend session.

The State Bank of Vietnam's transaction office continues to list the USD buying and selling price at 23,400 VND/USD and the spot selling rate at 25,450 VND/USD.

Interbank exchange rates during the week from December 23 to December 27 fluctuated in a downward trend at the beginning of the week and then increased again. At the end of the session on December 27, the interbank exchange rate closed at 25,455, unchanged from the previous weekend session.

The exchange rate on the free market increased sharply in the first two sessions of the week and then decreased again. At the end of the session on December 27, the free exchange rate increased slightly by 10 VND in both buying and selling directions compared to the previous weekend session, trading at 25,660 VND/USD and 25,760 VND/USD.

Interbank money market from December 23-27, interbank VND interest rates increased in the first 4 sessions of the week and then decreased again in the last session of the week. Closing on December 27, interbank VND interest rates were traded at: overnight 4.10% (+0.01 percentage point); 1 week 5.28% (+0.78 percentage point); 2 weeks 5.30% (+0.33 percentage point); 1 month 5.42% (+0.29 percentage point).

Interbank USD interest rates fluctuated little last week. On December 27, interbank USD interest rates were: overnight 4.44% (+0.01 percentage point); 1 week 4.50% (unchanged); 2 weeks 4.59% (+0.01 percentage point) and 1 month 4.62% (unchanged).

In the open market from December 23 to December 27, in the mortgage channel, the State Bank offered 7-day and 14-day terms with a volume of VND70,000 billion, with interest rates kept at 4.0%. There were VND69,999.91 billion in winning bids and VND3,999.93 billion maturing last week in the mortgage channel.

SBV bids for 7-day treasury bills. VND20,810 billion was won, with an interest rate of 4.0%. VND41,373 billion of treasury bills matured last week.

Thus, the State Bank of Vietnam pumped a net VND86,562.98 billion into the market last week through the open market channel. There were VND79,999.91 billion circulating on the mortgage channel, and VND64,890 billion of State Bank of Vietnam bills circulating on the market.

On the bond market on December 25, the State Treasury successfully bid for VND2,000 billion/VND7,000 billion of government bonds called for bid, with a winning rate of 29%. Of which, the 5-year term won VND800 billion/VND1,500 billion of the call, the 10-year term raised VND200 billion/VND3,500 billion of the call and the 30-year term raised the entire VND1,000 billion of the call. The 15-year and 20-year terms each called for VND500 billion but there was no winning volume. The winning interest rate for the 5-year term was 2.06% (+0.15 percentage points compared to the previous auction), the 10-year term was 2.77% (+0.11 percentage points) and the 30-year term was 3.22% (+0.12 percentage points).

This week, on January 2, the State Treasury plans to bid for VND7,000 billion in government bonds, of which VND1,500 billion will be offered for 5-year terms, VND3,500 billion for 10-year terms, VND1,000 billion for 15-year terms, and VND1,000 billion for 30-year terms.

The average value of Outright and Repos transactions in the secondary market last week reached VND18,064 billion/session, a sharp increase compared to VND14,238 billion/session of the previous week. Government bond yields last week continued to increase across all maturities. At the close of the session on December 27, government bond yields were trading around 1-year 1.97% (+0.03 percentage points compared to the session at the end of last week); 2-year 1.98% (+0.03 percentage points); 3-year 2.01% (+0.04 percentage points); 5-year 2.29% (+0.01 percentage points); 7-year 2.52% (+0.01 percentage points); 10-year 2.97% (+0.01 percentage points); 15-year 3.12% (+0.04 percentage points); 30 years 3.27% (+0.02 percentage points).

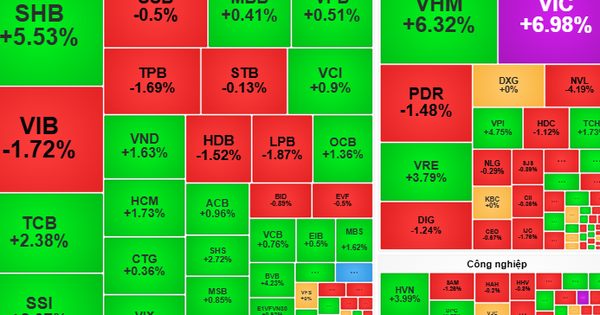

The stock market in the week from December 23 to December 27 had quite positive developments. At the end of the session on December 27, VN-Index stood at 1,275.14 points, up 17.64 points (+1.40%) compared to the previous weekend; HNX-Index added 2.06 points (+0.91%) to 229.13 points; UPCoM-Index increased 1.09 points (+1.17%) to 94.48 points.

Average market liquidity reached over VND18,300 billion/session, a positive increase from VND14,500 billion/session the previous week. Foreign investors continued to net sell nearly VND433 billion on all three exchanges.

International News

The US saw some important economic indicators. First, US durable goods orders fell 1.1% month-over-month in November after rising 0.3% in October, which was worse than the 0.3% decline expected. In addition, core durable goods orders fell 0.1% month-over-month in November after rising 0.2% in the previous month, which was contrary to expectations of a slight increase of 0.3%.

Next, the Conference Board survey said the US consumer confidence index was at 104.7 points in December, down sharply from 112.8 points in the previous month, and lower than the forecast of 112.9 points. In the real estate market, new home sales in November reached 664 thousand units, higher than 627 thousand units in October and almost matching the forecast of 666 thousand units.

Finally, in the labor market, the number of initial jobless claims in this country in the week ending December 20 was 219 thousand, down slightly from 220 thousand the previous week, contrary to the forecast of a slight increase to 223 thousand. The average number of claims in the most recent 4 weeks was 226.5 thousand, up 1 thousand compared to the average of the previous 4 weeks.

The World Bank (WB) has raised its economic outlook for China, while the country has also taken new economic stimulus measures. Specifically, the WB believes that thanks to the effectiveness of recent easing policies, China's GDP could reach a growth rate of 4.9% this year, slightly higher than the forecast of 4.8% in June. In 2025, the WB forecasts China's GDP to grow by only 4.5%, although it has been adjusted up from the previous forecast of 4.1%.

Also last week, China announced plans to issue a record 3 trillion yuan (about $411 billion) in special treasury bonds in 2025 to attract investment and support local governments. The size of the package far exceeds the 1 trillion the government issued in 2024.

In addition, the Chinese National People's Congress has just decided to extend the validity of value-added tax refunds until the end of 2027 to encourage domestic and foreign economic organizations to buy Chinese-made equipment. In 2019, China cut VAT for manufacturers from 16% to 13% and from 10% to 9% for the transportation and construction sectors. VAT accounts for about 38% of China's tax revenue in 2023.

VAT revenue for the first 11 months of 2024 fell 4.7% year-on-year to CNY6.1 trillion ($840 billion). However, recent months have seen a gradual recovery in tax revenue, with November alone recording a 1.36% year-on-year increase.

Source: https://thoibaonganhang.vn/diem-lai-thong-tin-kinh-te-tuan-tu-23-2712-159426-159426.html

![[Photo] Prime Minister Pham Minh Chinh receives Deputy Prime Minister of the Republic of Belarus Anatoly Sivak](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/2/79cdb685820a45868602e2fa576977a0)

![[Photo] Special relics at the Vietnam Military History Museum associated with the heroic April 30th](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/3/a49d65b17b804e398de42bc2caba8368)

![[Photo] Prime Minister Pham Minh Chinh receives CEO of Standard Chartered Group](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/2/125507ba412d4ebfb091fa7ddb936b3b)

![[Photo] Comrade Khamtay Siphandone - a leader who contributed to fostering Vietnam-Laos relations](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/3/3d83ed2d26e2426fabd41862661dfff2)

Comment (0)