The central exchange rate increased by 60 VND, the VN-Index decreased by 5.07 points compared to the previous weekend, or the market capitalization of stocks on the three exchanges HOSE, HNX and UPCoM on December 16 reached 7,085 trillion VND, up 19.3% compared to the end of last year... are some notable economic information in the week from December 16-20.

| Economic news review on December 18 Economic news review on December 19 |

|

| Economic news review |

Overview

Vietnam's stock market in 2025 has many positive signals.

As of December 20, 2024, the VN-Index reached 1,257.50 points, up over 11% compared to the end of the previous year. The market capitalization of stocks on the three exchanges HOSE, HNX and UPCoM on December 16 reached VND 7,085 trillion, up 19.3% compared to the end of the previous year, equivalent to 69.3% of estimated GDP in 2023, equivalent to a price-to-earnings ratio (P/E) of about 12 times.

Market liquidity remains high, with an average trading value of more than VND 21 billion per session, up 7.6% compared to the average in 2023. The total capital mobilized through the stock market accounts for about 14.5% of the total social investment capital. The number of investor accounts continues to increase, reaching more than 9.1 million accounts by the end of November 2024, equivalent to about 9% of the population, reaching the target of 9 million accounts ahead of schedule in 2025 and aiming for the number of 11 million accounts by 2030 as set out in the Stock Market Development Strategy to 2030 approved by the Government.

The bond market continued to recover with an average trading value of VND11,542 billion per session, up 77.1% compared to the average of the previous year. The listing scale continued to grow with 466 listed bond codes with a listing value of more than VND2,304 trillion, up 13.5% compared to 2023, equivalent to 22.5% of estimated GDP in 2023.

Experts believe that the Vietnamese stock market has not yet broken through at this point in 2024 for the following reasons. First of all, it is due to the strong volatility in the market when individual investors still account for more than 90%, while this group is very susceptible to psychological impacts. Moreover, since the beginning of 2024, foreign investors have net sold nearly VND 95,000 billion in the Vietnamese stock market, much higher than the level of about VND 22,000 billion last year. This is also a factor affecting the psychology of domestic investors, causing capital flows not to flow strongly into the market.

In addition, the unfinished upgrading story, the scarcity of new quality supply, the lack of new financial products... are the limitations that make it difficult for the market to develop as expected. For example, the most essential factor for the market is goods, especially new high-quality goods. However, in recent years, the roadmap to list Agribank, MobiFone, TKV, VNPT... on the stock exchange has remained quiet; VNPT was expected to IPO at the end of 2019 with 35% of shares offered to investors, but so far there has been no progress...

In 2025, experts predict that Vietnam's economy will continue to face a number of challenges due to changes in the international economic context, through which the Vietnamese stock market is forecast to have more large fluctuations but still in an upward trend. For the stock market to develop sustainably, it is important to increase new goods, new products and upgrade the market.

Regarding market upgrading, measures to resolve obstacles to upgrade the Vietnamese stock market are being vigorously implemented. The regulation that foreign institutional investors can trade to buy shares without requiring sufficient funds (Non Pre-funding solution - NPS) has been officially applied since November 2, 2024. This is one of the two important conditions for FTSE Russell to consider upgrading that the Vietnamese stock market is lacking. Next will be to resolve obstacles regarding the ownership ratio of foreign investors. It is possible that the Vietnamese stock market will be considered for upgrading by FTSE in the September 2025 assessment period and officially upgraded at the end of 2026.

Domestic market summary week from December 16-20

In the foreign exchange market, during the week of December 16-20, the central exchange rate was adjusted up by the State Bank in most sessions, especially increasing sharply in the last two sessions of the week. At the end of December 20, the central exchange rate was listed at 24,324 VND/USD, a sharp increase of 60 VND compared to the previous weekend session.

The State Bank of Vietnam's transaction office continues to list the buying and selling prices at 23,400 VND/USD and the spot selling rate at 25,450 VND/USD.

The interbank USD-VND exchange rate in the week from December 16 to December 20 fluctuated in an upward trend. At the end of the session on December 20, the interbank exchange rate closed at 25,455, up 52 VND compared to the previous weekend session.

The dollar-dong exchange rate on the free market increased in most sessions last week. At the end of the session on December 20, the free exchange rate increased by 100 VND in both buying and selling directions compared to the previous weekend session, trading at 25,650 VND/USD and 25,750 VND/USD.

Interbank money market, week from December 16-20, interbank VND interest rates decreased in the first 4 sessions of the week and increased sharply in the last session of the week. Closing on December 20, interbank VND interest rates were traded at: overnight 4.09% (+0.01 percentage point); 1 week 4.50% (+0.07 percentage point); 2 weeks 4.97% (+0.39 percentage point); 1 month 5.13% (+0.01 percentage point).

Interbank USD interest rates decreased in all terms. On December 20, the interbank USD interest rate was traded at: overnight 4.43% (-0.18 percentage points); 1 week 4.50% (-0.16 percentage points); 2 weeks 4.58% (-0.13 percentage points) and 1 month 4.62% (-0.13 percentage points).

In the open market last week from December 16 to December 20, in the mortgage channel, the State Bank of Vietnam offered 7-day and 14-day terms with a volume of VND14,000 billion, with interest rates kept at 4.0%. There were VND13,999.93 billion in winning bids and VND50,999.89 billion maturing last week in the mortgage channel.

SBV bids for treasury bills SBV bids for interest rates at 3 terms: 7 days, 14 days and 28 days. VND16,643 billion won the bid for the 7-day term, with an interest rate of 4.0%, VND28,200 billion won the bid for the 14-day term, with an interest rate of 4.0% and VND5,580 billion won the bid for the 28-day term, with an interest rate of 4.0%. VND15,975 billion of treasury bills matured last week.

Thus, the State Bank of Vietnam net withdrew VND 71,447.96 billion from the market last week through the open market channel. There were VND 13,999.93 billion circulating on the mortgage channel, and VND 85,453 billion in State Bank bills circulating on the market.

Bond market, on December 18, the State Treasury successfully bid VND829 billion/VND9,000 billion of government bonds called for bid, with a winning rate of 9%. Of which, the 5-year term won VND100 billion/VND2,000 billion called for bid, the 10-year term raised VND300 billion/VND4,500 billion called for bid and the 30-year term raised VND429 billion/VND1,500 billion called for bid. The 15-year term alone called for VND1,000 billion but there was no winning volume. The winning interest rate for the 5-year term was 2.0% (+0.09 percentage points compared to the previous auction), the 10-year term was 2.75% (+0.09 percentage points) and the 30-year term was 3.18% (+0.08 percentage points).

This week, on December 25, the State Treasury plans to bid for VND7,000 billion in government bonds, of which VND1,500 billion will be offered for the 5-year term, VND3,500 billion for the 10-year term, VND500 billion for the 15-year term, VND500 billion for the 20-year term, and VND1,000 billion for the 30-year term.

The average value of Outright and Repos transactions in the secondary market last week reached VND14,238 billion/session, a sharp decrease compared to VND29,255 billion/session of the previous week. Government bond yields last week increased sharply across all maturities. At the close of the session on December 20, government bond yields were trading around 1-year 1.94% (+0.08 percentage points compared to the session at the end of last week); 2-year 1.95% (+0.08 percentage points); 3-year 1.98% (+0.08 percentage points); 5-year 2.29% (+0.15 percentage points); 7-year 2.51% (+0.14 percentage points); 10-year 2.97% (+0.12 percentage points); 15-year 3.08% (+0.06 percentage points); 30-year 3.25% (+0.06 percentage points).

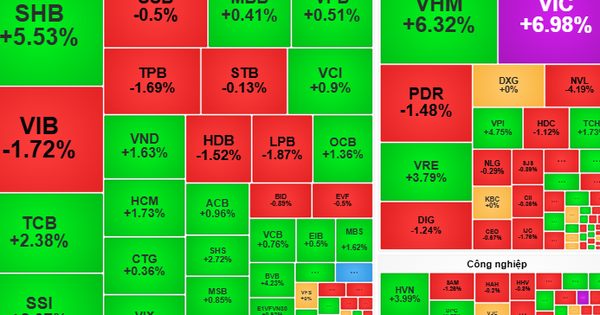

Stock market, week from December 16 to December 20, the stock market traded slowly, showing the hesitant psychology of investors. At the end of the session on December 20, VN-Index stood at 1,257.50 points, down 5.07 points (-0.40%) compared to the previous weekend; HNX-Index inched up 0.07 points (+0.03%) to 227.07 points; UPCoM-Index increased 0.85 points (+0.92%) to 93.39 points.

Average market liquidity reached over VND14,500 billion/session, down slightly from VND15,100 billion/session the previous week. Foreign investors continued to net sell over VND1,915 billion on all three exchanges.

International News

The US Federal Reserve (Fed) updated its economic outlook and policy interest rates last week, while the US received a number of important economic indicators. At its meeting on December 17-18, the Fed forecast US GDP growth of 2.5% and 2.1% in 2024 and 2025, respectively, both higher than the forecast of 2.0% growth in September. The unemployment rate is forecast at 4.2% this year and slightly up to 4.3% next year, both lower than the previous forecast of 4.4%.

On inflation, the Fed forecasts the headline PCE price index to rise 2.4% this year and 2.5% in 2025, down from its previous forecasts of 2.3% and 2.1%, respectively. Core PCE is forecast to rise 2.8% and 2.5% in 2021, still decelerating but more persistently than the September forecasts of 2.6% and 2.2%.

Regarding the policy interest rate, in this meeting, the Federal Open Market Committee (FOMC, under the Fed) decided to cut another 25 basis points, from 4.50% - 4.75% to 4.25% - 4.5%. Throughout 2024, the Fed has cut the policy interest rate three times with a total of 100 basis points, starting from September. The Fed forecasts that it will only cut the interest rate by another 50 basis points in 2025 instead of 100 basis points as previously forecast, bringing the policy interest rate down to 3.75% - 4.0% by the end of next year.

Regarding the US economy, the US Bureau of Statistics announced that the official GDP increased by 3.1% compared to the previous quarter in the third quarter, revised higher than the 2.8% increase according to the initial statistical results. Regarding inflation, the core PCE consumer price index increased by 0.1% compared to the previous month in November, slowing down from the 0.3% in October and at the same time lower than the forecast increase of 0.2%. Compared to the same period in 2023, the core PCE increased by 2.8% compared to the same period in 2023, unchanged from the increase recorded in October.

In the labor market, the number of initial jobless claims in the US in the week ending December 14 was 220 thousand, down from 242 thousand the previous week and also lower than the forecast of 229 thousand. The average number of claims in the last 4 weeks was 225.5 thousand, up 1.25 thousand compared to the previous 4 weeks.

Finally, total retail sales in the country increased 0.7% month-on-month in November after increasing 0.5% in October, beating the forecast of 0.6% increase. Compared to the same period in 2023, total retail sales increased 3.8% year-on-year, faster than the 2.9% increase in October, also the strongest increase since December 2023.

The Bank of England (BoE) left its policy rate unchanged at its year-end meeting. At its meeting on December 19, the BoE said that its CPI inflation rate in November rose to 2.6% from 1.7% in October, mainly due to the price of core goods and food.

In addition, service inflation remains high. The BoE believes that inflation may continue to increase slightly in the coming time. The Monetary Policy Committee (MPC, under the BoE) affirmed its determination to pursue the inflation target of 2.0% while maintaining employment growth. In this meeting, the MPC decided to keep the policy interest rate unchanged at 4.75% with the consensus of 6/9 members. The remaining 3 members supported a 25 basis point cut in the policy interest rate. The MPC will continue to rely on inflation and economic data in the following meetings to make appropriate decisions on the direction of monetary policy.

In terms of the UK economy, headline and core CPI rose 2.6% and 3.5% year-on-year in November, up from 2.3% and 3.3% in October, and in line with forecasts of 2.6% and 3.6%. These are both the highest increases in the second half of 2024.

On the labor market, the number of unemployment benefit applications in the UK increased slightly by 0.3 thousand applications in November after falling by 10.9 thousand in October, much lower than the Reuters forecast of an increase of 28.2 thousand applications.

Next, the average income of the British people increased by 5.2% in the 3 months of 09-10-11, higher than the increase of 4.4% in the 3 months of 08-09-10, and also higher than the expected increase of 4.6%. Finally, the unemployment rate in the UK last month was recorded at 4.3%, unchanged from the statistical results of October and also in line with the forecast.

Source: https://thoibaonganhang.vn/diem-lai-thong-tin-kinh-te-tuan-tu-16-2012-159225-159225.html

![[Photo] Prime Minister Pham Minh Chinh receives Deputy Prime Minister of the Republic of Belarus Anatoly Sivak](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/2/79cdb685820a45868602e2fa576977a0)

![[Photo] Prime Minister Pham Minh Chinh receives CEO of Standard Chartered Group](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/2/125507ba412d4ebfb091fa7ddb936b3b)

![[Photo] Special relics at the Vietnam Military History Museum associated with the heroic April 30th](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/3/a49d65b17b804e398de42bc2caba8368)

![[Photo] Comrade Khamtay Siphandone - a leader who contributed to fostering Vietnam-Laos relations](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/3/3d83ed2d26e2426fabd41862661dfff2)

Comment (0)