Banks are facing the risk of a decline in net interest margins (NIMs) due to pressure to reduce lending rates, while deposit rates are unlikely to fall sharply. To maintain efficiency, they need to further optimize operating costs.

Profits likely to stagnate

Since the meeting between the State Bank of Vietnam (SBV) and banks in late February 2025, more than 20 commercial banks have reduced their deposit interest rates. However, the reductions have mainly been applied to certain terms and focused on regular customers, while deposit interest rates for VIP customers - which account for a large proportion of the deposit structure of many banks - have remained almost unchanged. Therefore, the input capital costs of many banks have not decreased significantly.

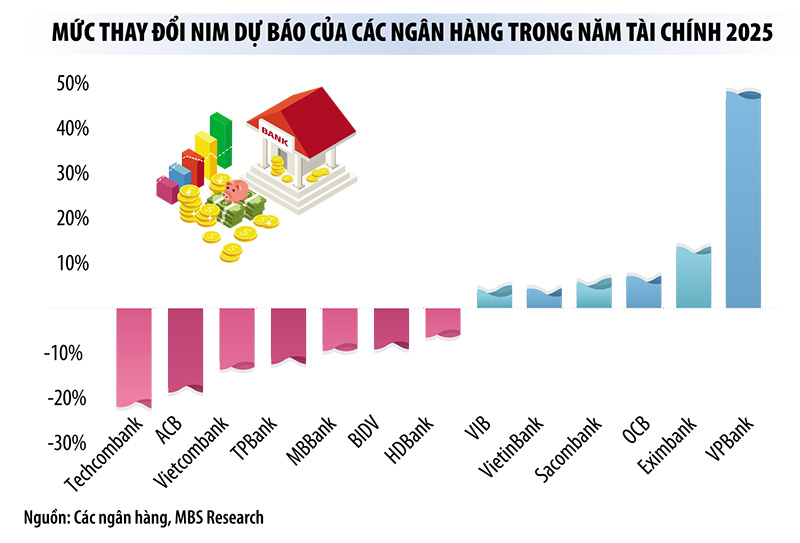

To support the economic growth target of 8% or more this year, many banks have launched credit packages with preferential interest rates. However, when output interest rates decrease while input interest rates have not decreased significantly, the net interest margin (NIM) and profits of the banking industry this year may be under pressure.

According to experts from MBS Securities Company, credit in 2025 is forecast to increase sharply (17-18%), while capital mobilization increases slowly, putting pressure on bank liquidity. Therefore, capital costs in 2025 are unlikely to decrease compared to 2024. Regarding lending interest rates, banks are likely to continue to maintain low levels to support customers due to increasingly fierce competition in the credit sector.

“With the pressure to increase deposit interest rates in the coming quarters, banks’ NIMs are unlikely to increase sharply in 2025,” MBS experts said. Therefore, MBS has adjusted its forecast for industry-wide profit growth from 20.2% to 17.7%, equivalent to the growth rate in 2024, even though credit is expected to increase higher this year.

Deputy Governor of the State Bank of Vietnam Dao Minh Tu emphasized that the decision on deposit and lending interest rates is up to commercial banks. However, in the current context, banks need to share difficulties with businesses, considering businesses as important partners in the financial ecosystem. When businesses encounter difficulties, banks also need to accompany and support them.

Experts say that banks are currently the most profitable group of enterprises in the Vietnamese economy. Although banks have recently adjusted their NIM to support the economy, the reduction is still insignificant due to profit pressure. However, with the liquidity support policies from the State Bank, there is still room to reduce lending rates.

The State Bank of Vietnam leader affirmed that banks do not need to worry too much about competition in deposit interest rates, because the State Bank of Vietnam will have many solutions to support liquidity through the interbank market.

Optimize costs, increase non-interest income

Currently, banks still rely heavily on credit activities, with about 80% of their income coming from this source. Therefore, when net interest margins (NIM) slow down, banks' profit growth is also significantly affected. To maintain growth momentum, banks are forced to accelerate cost optimization, seek cheaper sources of capital, and expand non-interest income sources.

According to Mr. Le Hoai An, CFA expert at Wiresearch, in the context of low interest rates, increasing competitive pressure makes the problem of optimizing mobilization costs become a decisive factor in the ability to improve NIM. Banks with the advantage of cheap capital sources and diversified mobilization channels will have more opportunities to adapt more flexibly to low lending interest rates.

Recently, some banks have launched "super-yield" deposit products to attract deposits under 1 month. Instead of only applying a non-term interest rate of 0.1%/year, many banks have set up flexible deposit terms, even from 1 day, with interest rates up to 2.5%/year - dozens of times higher than the non-term interest rate. This move takes place in the context of increasingly fierce competition for CASA (non-term deposits), when this capital flow is decreasing at many banks.

In addition, to offset the slowdown in NIM, many banks are focusing on digital transformation and streamlining staff to optimize operating costs.

It can be seen that the recent growth in bank profits does not simply come from enjoying interest rate differences, but also thanks to promoting digitalization and effective cost control.

In addition, increasing non-interest income is also an important solution. In 2024, the growth rate of interest income of banks is significantly lower than the growth rate of non-interest income. According to forecasts of analysts at MBS, interest income of banks this year is expected to increase by about 17%, mainly due to the low comparison base of the previous year. However, the proportion of non-interest income to total operating income is still only about 22%.

Finally, bank profit growth this year also depends on provisioning costs. The credit expansion may lead to an increase in bad debts, forcing banks to increase their provisioning – expected to increase by nearly 17% this year. Accordingly, only banks that maintain credit quality can ensure stability in profit growth.

Source: https://baodaknong.vn/ngan-hang-chat-vat-tim-giai-phap-cat-giam-chi-phi-van-hanh-246699.html

![[Photo] Special relics at the Vietnam Military History Museum associated with the heroic April 30th](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/3/a49d65b17b804e398de42bc2caba8368)

![[Photo] Comrade Khamtay Siphandone - a leader who contributed to fostering Vietnam-Laos relations](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/3/3d83ed2d26e2426fabd41862661dfff2)

![[Photo] Prime Minister Pham Minh Chinh receives CEO of Standard Chartered Group](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/2/125507ba412d4ebfb091fa7ddb936b3b)

![[Photo] Prime Minister Pham Minh Chinh receives Deputy Prime Minister of the Republic of Belarus Anatoly Sivak](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/2/79cdb685820a45868602e2fa576977a0)

Comment (0)