Stock Market Perspective Week 8-13/4: Short-term risks tend to increase

The market is now more inclined towards short-term speculation, suitable for positions that have sold at high prices and bought back at low prices. New buying positions need to be evaluated and selected more carefully.

The first week of April saw a lackluster performance on the stock market, with the VN-Index falling as it faced increasing selling pressure right after approaching the strong resistance zone around 1,290 - 1,300 points. Cash flow seemed to be selective in stocks as there was no specific industry group leading the way.

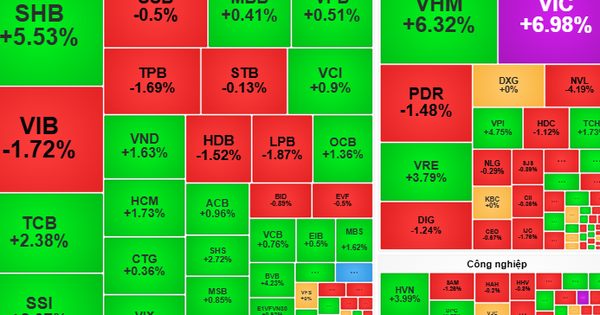

The bright spots came from real estate and oil and gas stocks. Meanwhile, the correction was strong in the banking group and other pillar stocks such as HPG and FPT.

Specifically, the banking group became the biggest pressure causing the VN-Index to decline during the week. This group occupied the top 4 positions in terms of negative impact on the index including CTG, BID, MBB and TCB, taking away a total of 10.3 points from the VN-Index. In addition, in the top 10 there were other banking codes such as ACB, VIB and STB. In terms of increasing points, HVN and NVL with increases of 15.2% and 6% respectively led the group of positive impacts on the VN-Index.

At the end of the week, VN-Index decreased by 2.23% compared to the previous week to 1,255.11 points, returning to test the highest price zone in 2023, corresponding to 1,245 points - 1,255 points. VN-Index is still surpassing important medium- and long-term resistance zones such as 1,200 points and 1,250 points.

During the week, liquidity on HoSE reached VND127,065 billion, up 12.4% compared to the previous week. Foreign investors continued to net sell with a value of VND2,182 billion. Compared to previous weeks, this week foreign investors were less negative when they net bought again in the last 2 sessions of the week, although with a small value. The top net sellers of the week were VHM (VND654 billion), MSN (VND526 billion) and SSI (VND491 billion). Meanwhile, the leading net buyers were MWG with a value of VND391 billion and NVL (VND201 billion).

According to Mr. Phan Tan Nhat, Head of Analysis at SHS Securities Company, some reasons negatively impacted the market last week, such as (1) The exchange rate increased sharply. (2) Government bond yields increased and are escaping the downtrend that has lasted from October 2022 to present. Vietnam's 10-year bonds last week at one point reached 2.92%, a sharp increase from 2.3% in early January 2024, affecting cash flow into the stock market. In addition, after 5 months of price increase, many codes/code groups have increased sharply with an increase of 50-100%, leading to profit-taking pressure.

Last week, the market was strongly differentiated, the positive point is that the medium-term cash flow is still maintained in the market and circulates well, such as increasing in oil and gas stocks when many codes after a 5-6 month accumulation period have increased sharply in price last week, or codes in the real estate group. However, most of them are under pressure to take profits and sell strongly after a period of good price increase, such as banking, industrial park, and securities codes.

Notable information of the week, according to data from the Vietnam Securities Depository (VSD), the number of domestic investor accounts increased by 163,621 accounts in March 2024, the number of new openings is increasing in the context of falling interest rates, continuously increasing gold prices, the real estate industry is still struggling, bonds have not regained confidence, so securities are the top choice.

In addition, other positive information is that Vietcombank officially adjusted savings interest rates. For individual customers, VCB adjusted down 0.1 percentage points for terms from 1 month to 9 months. For institutional customers, Vietcombank also adjusted down the average savings interest rate by 0.1 percentage points for terms from 1 to 12 months.

Technically, after failing to rise back to the old peak at 1,290, the VN-Index has fallen decisively for three consecutive sessions, which is a worrying sign for the short-term trend.

The psychological support level of 1,250 points may help the index to be more balanced next week, but to escape the short-term downtrend, the VN-Index needs time to stabilize and create a foundation. Investors need to carefully observe the index's developments at the 1,250 point mark and possibly at the 1,230 point mark, if the VN-Index has not stopped falling. It is important to note that market risks are on the rise.

Trading strategy next week, short-term investors focus on managing positions and keeping stock proportions at a balanced level, can consider increasing stocks gradually during the correction phase.

With long-term capital, investors continue to hold stocks with good fundamentals and positive prospects for target prices. Investors with high cash ratio can consider the short-term support zone of 1,250 points to increase their positions.

The industries to be monitored are real estate, oil and gas, exports, consumer goods, and steel and galvanized steel.

Mr. Nhat predicts that next week, the market will continue to differentiate strongly, codes and groups of codes under selling pressure will recover and accumulate, while short-term and speculative cash flow may continue to increase in codes that have had positive developments in the past week. If the VN-Index continues to be under selling pressure, it will recover to create a balanced bottom at the price range of around 1,240 points and accumulate in the price range of 1,240-1,245 to 1,265-1,270 points.

However, the market is currently more inclined towards short-term speculation, suitable for positions that have sold at high prices and bought back at low prices. New buying positions need to be evaluated more carefully and selectively, gradually accumulating good quality stocks that have been under strong downward pressure in the past week, such as industrial park, seaport, and energy stocks.

From a cautious investment perspective, Mr. Nhat said that investors should wait for information to be announced (1) The situation of total margin debt, total available money of investors in companies at the end of the first quarter of 2024 to make a more thorough assessment. It is expected that the total margin debt at the end of the first quarter could reach 195,000 - 200,000 billion VND, accounting for a fairly high proportion. (2). It is necessary to wait for information on business results in the first quarter of 2024 to be announced, to evaluate the business performance, cash flow, and balance sheet of interested businesses, before making new investment decisions.

Source

![[Photo] Unique folk games at Chuong Village Festival](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/10/cff805a06fdd443b9474c017f98075a4)

![[Photo] Prime Minister Pham Minh Chinh chairs meeting to discuss tax solutions for Vietnam's import and export goods](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/10/19b9ed81ca2940b79fb8a0b9ccef539a)

![[Photo] Phuc Tho mulberry season – Sweet fruit from green agriculture](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/10/1710a51d63c84a5a92de1b9b4caaf3e5)

Comment (0)