The central exchange rate decreased by 44 VND, the VN-Index increased by 22.36 points compared to the previous weekend, or the pressure to disburse public investment capital in the remaining time of the 2024 budget year is still very large... are some notable economic information in the week from November 25-29.

| Review of economic information on November 28 Prime Minister directs to strengthen credit management solutions in 2024 |

|

| Economic news review |

Overview

The pressure to disburse public investment capital in the remaining time of the 2024 budget year is still very large.

The 2024 state budget investment plan assigned by the Prime Minister to ministries, central and local agencies is VND 680,075.8 billion, including: central budget capital of VND 247,726.9 billion, local budget capital of VND 432,348.9 billion. In addition, the 2024 local budget balance capital assigned by localities increased compared to the plan assigned by the Prime Minister, updated to the end of November 2024, at VND 70,019.1 billion; the capital plan of previous years allowed to be extended up to the time of reporting is VND 56,807.2 billion. Thus, the total plan assigned in 2024 up to November 30 is VND 806,902.1 billion.

According to the report of the Ministry of Finance, the estimated disbursement of public investment capital by the end of November 2024 is VND 438,852.7 billion, reaching 54.4% of the overall plan, reaching 64.52% of the plan assigned by the Prime Minister. The estimated disbursement rate in the first 11 months of 2024 is lower than the same period last year (the same period in 2023 reached 59.4% of the plan and reached 65.1% of the plan assigned by the Prime Minister).

According to the Ministry of Finance, there are still difficulties and problems affecting the disbursement progress that have not been completely resolved, such as: problems related to policies and mechanisms; site clearance, land use planning and material supply; problems in completing investment procedures, disbursement processes of ODA projects, etc. that need to be actively and proactively resolved by ministries, branches, localities and investors to speed up the disbursement progress of public investment capital. In particular, the biggest difficulty that will arise in 2024 is common materials for the construction of large projects, especially traffic projects.

To achieve a public investment disbursement rate of over 95% as planned by the Prime Minister, in the remaining 2 months of the 2024 budget year (up to January 31, 2025), the whole country needs to disburse about 207 trillion VND (equivalent to about 30% of the plan assigned by the Prime Minister). Facing the possibility of not completing the 2024 public investment disbursement plan, on November 7, 2024, the Prime Minister issued Official Dispatch No. 115/CD-TTg on resolutely implementing tasks and solutions to promote public investment disbursement in the last months of 2024. Some key groups of solutions from now until the end of the year include:

(i) continue to implement the proposed solutions that have been issued by the Government and the Prime Minister, emphasizing the solution on urging and directing. The Prime Minister has directed the establishment of 7 Government Working Groups headed by Deputy Prime Ministers and 2 Ministers of Finance and Planning and Investment to urge disbursement; promote the mechanism of Government members working with localities to urge disbursement of public investment capital; (ii) organize implementation, this is a group of quite difficult solutions whose main responsibility belongs to ministries, branches and localities; (iii) remove difficulties: in addition to difficulties in common materials, there are other difficulties for some projects such as procedures, especially project adjustment procedures; (iv) strengthen discipline and order in public investment, especially promoting the application of information technology to manage public investment as quickly and effectively as possible.

In addition, according to the Ministry of Planning and Investment, the breakthrough solution to promote long-term public investment disbursement is identified as an institutional solution. The Law on Public Investment (amended) was submitted to the National Assembly at the 8th Session of the 15th Term, along with the amendment of 4 laws related to investment, including the Law on Planning, the Law on Investment, the Law on Investment under the public-private partnership model and the Law on Bidding. The market expects that the amended Laws, when coming into effect, will contribute to thoroughly resolving current problems and backlogs. Specifically, regarding the draft Law on Public Investment (amended), 05 major groups of amended policies in the proposal dossier in the Law Project include: (i) a group of policies to institutionalize pilot and specific mechanisms and policies permitted by the National Assembly to be applied; (ii) a group of policies on continuing to promote decentralization and delegation of power; (iii) policy group on improving the quality of investment preparation, resource exploitation, and capacity to implement public investment projects of localities and state-owned enterprises; (iv) policy group on promoting the implementation and disbursement of ODA capital plans and preferential loans from foreign donors; (v) policy group on simplifying procedures; supplementing and clarifying concepts, terms, and regulations, ensuring consistency and unity of the legal system.

Domestic market summary week from November 25-29

In the foreign exchange market, during the week of November 25-29, the central exchange rate was adjusted by the State Bank in a downward trend, especially sharply decreasing in the last 2 sessions of the week. At the end of November 29, the central exchange rate was listed at 24,251 VND/USD, a sharp decrease of 44 VND compared to the previous weekend session.

The State Bank of Vietnam's transaction office continues to list the USD buying and selling rates at 23,400 VND/USD and 25,450 VND/USD, respectively.

The interbank USD-VND exchange rate in the week from November 25 to November 29 gradually decreased over the sessions. At the end of the session on November 29, the interbank exchange rate closed at 25,372, down 60 VND compared to the session at the end of the previous week.

The dollar-dong exchange rate on the free market increased sharply at the beginning of the week and then decreased slightly again. At the end of the session on November 29, the free exchange rate increased by 40 VND in both buying and selling directions compared to the previous weekend session, trading at 25,690 VND/USD and 25,790 VND/USD.

Interbank money market, week from November 25-29, interbank VND interest rates continued to decrease sharply across sessions in all terms. Closing on November 29, interbank VND interest rates were traded at: overnight 3.13% (-1.47 percentage points); 1 week 3.90% (-0.86 percentage points); 2 weeks 4.49% (-0.37 percentage points); 1 month 4.79% (-0.19 percentage points).

Interbank USD interest rates fluctuated slightly across all terms last week. On November 29, interbank USD interest rates were: overnight 4.60% (unchanged); 1 week 4.67% (+0.01 percentage point); 2 weeks 4.71% (+0.01 percentage point) and 1 month 4.76% (unchanged).

In the open market last week from November 25 to November 29, in the mortgage channel, the State Bank of Vietnam offered 7-day term with a volume of VND54,000 billion, interest rate kept at 4.0%. There were VND53,999.85 billion in winning bids, VND68,000 billion maturing last week in the mortgage channel.

The State Bank of Vietnam bid for 28-day State Bank bills, bidding for interest rates. There were 9,980 billion VND in winning bids, interest rates remained at 4.0%. There were 7,950 billion VND in bills maturing last week.

Thus, the State Bank of Vietnam net withdrew VND16,030.15 billion from the market last week through the open market channel. There were VND53,999.85 billion circulating on the mortgage channel, and VND20,080 billion of State Bank of Vietnam bills circulating on the market.

Bond market, November 27, the State Treasury successfully bid 4,000 billion VND/10,500 billion VND of government bonds called for bid, the winning rate reached 38%. Of which, the 10-year term mobilized 3,000 billion VND/5,500 billion VND of the call and the 30-year term mobilized 1,000 billion VND/1,500 billion VND of the call. The 5-year and 15-year terms called for bids of 2,500 billion VND and 1,000 billion VND respectively, but there was no winning volume in either term. The winning interest rate for the 10-year term was 2.68% (+0.02 percentage points compared to the previous auction) and for the 30-year term was 3.15% (+0.05 percentage points).

This week, on December 4, the State Treasury plans to bid for VND9,000 billion in government bonds, of which VND1,500 billion will be offered for 5-year terms, VND5,000 billion for 10-year terms, VND1,000 billion for 15-year terms, and VND1,500 billion for 30-year terms.

The average value of Outright and Repos transactions in the secondary market last week reached VND16,072 billion/session, a sharp increase compared to VND13,878 billion/session of the previous week. Government bond yields last week fluctuated slightly across all maturities. At the close of the session on November 29, government bond yields were trading around 1-year 1.85% (+0.004 percentage points compared to the session at the end of last week); 2-year 1.86% (+0.004 percentage points); 3-year 1.88% (+0.004 percentage points); 5-year 1.97% (+0.003 percentage points); 7-year 2.28% (-0.001 percentage points); 10-year 2.76% (unchanged); 15-year 2.96% (+0.001 percentage points); 30-year 3.16% (unchanged).

Stock market, week from November 25 to November 29, the stock market performed quite positively when all 3 indices closed the week in green. At the end of the session on November 29, VN-Index stood at 1,250.46 points, up 22.36 points (+1.82%) compared to the previous weekend; HNX-Index added 3.35 points (+1.51%) to 224.64 points; UPCoM-Index increased 1.04 points (+1.13%) to 92.74 points.

Average market liquidity reached about VND12,900 billion/session, down from VND15,000 billion/session the previous week. Foreign investors net sold slightly nearly VND222 billion on all three exchanges.

International News

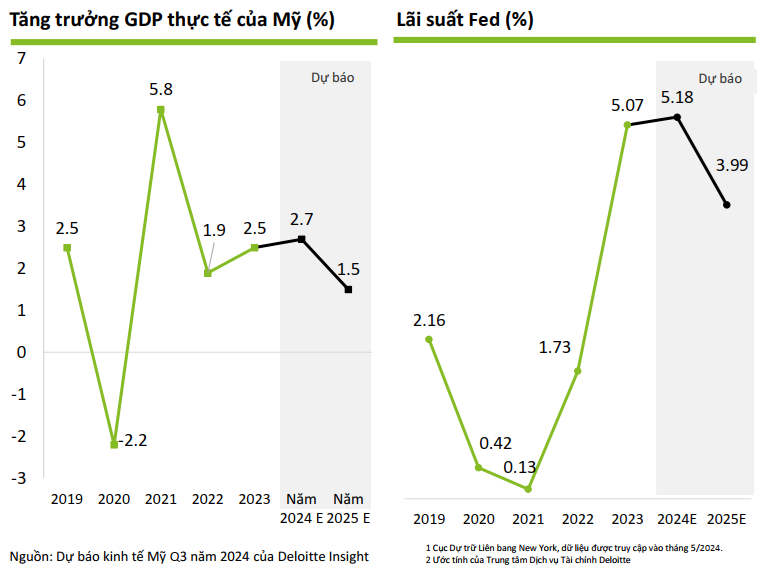

The Fed released the minutes of its November meeting, and the US recorded important economic indicators. In the minutes of the meeting released on November 26, the Fed noted that GDP growth has been solid since the beginning of the year. Job growth has slowed significantly, the real unemployment rate has increased but remains low. Consumer price inflation is much lower than what was recorded in 2023. The total PCE and core PCE price indexes in September were 2.1% and 2.7%, respectively, compared to the same period last year.

The Fed forecasts that US GDP will grow slightly below potential from 2025 to 2027, leading to a slight increase in the unemployment rate. Inflation is forecast to continue to slow as supply and demand in the market gradually balance out.

Regarding monetary policy, members of the Federal Open Market Committee (FOMC) of the Fed believed that the decision to begin easing monetary policy in September was appropriate, and that risks to achieving the employment and inflation goals were roughly balanced. To support these goals, the FOMC decided to lower the policy rate by 25 basis points, from 4.75% - 5.0% to 4.50% - 4.75%. The FOMC will continue to rely on future economic data to make further decisions.

Regarding the US economy, the country's GDP increased by 2.8% compared to the previous quarter in the third quarter according to the second preliminary report, without adjusting the initial statistical results and matching the forecast.

Regarding US inflation, the core PCE and total PCE price indexes in the country both increased 0.3% month-on-month in October, equal to the increase in the previous month and matching the forecast.

Compared to the same period in 2023, core PCE and total PCE increased 2.8% and 2.3% respectively in October, both expanding from the 2.7% and 2.1% increases recorded in September.

In the housing market, U.S. pending home sales rose 2.0% month over month in October, following a 7.5% increase in the previous month and beating forecasts for a 2.1% decline. Pending home sales rose 7.0% year over year in October. The median home price in the U.S. rose 0.7% month over month in September, following a 0.4% increase in the previous month and beating forecasts for a 0.3% increase.

Thus, housing prices in this country in the third quarter increased by about 0.7% compared to the previous quarter and increased by 4.3% compared to the same period in 2023.

Finally, on the labor market, the number of initial unemployment claims in the US for the week ending November 22 was 213 thousand, contrary to the forecast of 215 thousand in the previous week. The average number of claims in the last 4 weeks was 217 thousand, down slightly by 1.25 thousand compared to the average of the previous 4 weeks. This week, the market is waiting for the detailed report on the US labor market in November, which will be announced on December 6, Vietnam time.

The Eurozone received some important economic news. First, on inflation, the Eurozone headline CPI rose 2.3% year-on-year in November, according to preliminary data, up from 2.0% in the previous month and in line with forecasts. The core CPI rose 2.7% year-on-year last month, flat from October and against forecasts for a slight increase to 2.8%.

In Germany alone, the CPI in November fell slightly by 0.2% month-on-month after rising 0.4% in the previous month, matching forecasts. Compared to the same period in 2023, the German CPI rose 2.2% year-on-year in November, up from a 2.0% increase in October. Finally, the Ifo survey organization said that the German business confidence index stood at 85.7 points in November, down from 86.5 points in October and below forecasts at 86.1 points.

This week, the Eurozone awaits information related to the labor market and retail sales for October, announced on December 2 and 5, respectively, Vietnam time.

Source: https://thoibaonganhang.vn/diem-lai-thong-tin-kinh-te-tuan-25-2911-158326.html

![[Photo] Unique folk games at Chuong Village Festival](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/10/cff805a06fdd443b9474c017f98075a4)

![[Photo] Prime Minister Pham Minh Chinh chairs meeting to discuss tax solutions for Vietnam's import and export goods](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/10/19b9ed81ca2940b79fb8a0b9ccef539a)

![[Photo] Phuc Tho mulberry season – Sweet fruit from green agriculture](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/4/10/1710a51d63c84a5a92de1b9b4caaf3e5)

Comment (0)