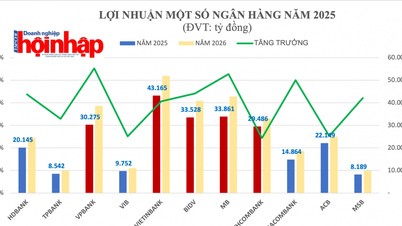

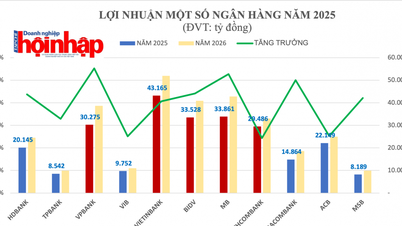

The report notes positive developments from Techcombank with stable growth in profits, market capitalization, and asset quality.

Techcombank was rated 'BB-' and given a 'stable' outlook by S&P Global Ratings - Photo: Techcombank

Recognizing Positive Developments from Techcombank: Vietnam Technological and Commercial Joint Stock Bank ("Techcombank" or TCB) has been awarded its 2024 annual rating by S&P Global Ratings ("S&P"), reaffirming its "BB-" issuer rating and "stable" outlook, higher than the "b+" anchor rating of the Vietnamese banking industry. The report acknowledges Techcombank's positive developments, including stable profit growth, market capitalization, and asset quality, a diversified deposit base, and low-cost management thanks to technological and product innovations. In this assessment, S&P emphasized its belief that Techcombank is likely to maintain above-average profitability alongside stable market capitalization and asset quality. The rating agency also expressed the view that Techcombank's large, low-cost, and stable deposit base will help mitigate risks associated with wholesale funding sources during market volatility. According to S&P, the "stable" outlook reflects the view that Techcombank will maintain its "strong network of funding and above-average profitability over the next 12-18 months." Furthermore, S&P affirms its confidence in the bank's continued superior profitability, contributing to its above-average credit growth rate. Techcombank is recognized as a bank generating exceptional returns, with a core return on total assets of 3% over the past four years, significantly higher than the industry average of 1-1.5%. The drivers of this outstanding performance, as acknowledged by S&P, are its "high-margin loan portfolio, large proportion of low-cost funding, and substantial non-interest income." "We are pleased that credit rating agency S&P has recognized the progress the Bank has made in a number of areas: superior profitability, stable capitalization and asset quality, diversified deposit base and low costs supported by technological and product innovation." While both the rating and outlook have been maintained, S&P's latest rating update takes a more positive view of the bank's operating environment, reflecting both Vietnam's high GDP growth rate and the quality of the bank's credit portfolio, after maintaining very healthy quality during the real estate market slowdown over the past two years. S&P has also adjusted its rating upgrade scenario for Techcombank, with criteria consistent with the Bank's publicly announced credit orientation, particularly regarding further portfolio diversification in the future," said Alex Macaire, Group Chief Financial Officer. Techcombank is among the top banks with the highest non-performing loan (NPL) levels. lowest in the system

Techcombank consistently ranks among the top banks with the lowest levels of non-performing loans and loans requiring attention in the entire banking system - Photo: Techcombank

Regarding asset quality, S&P expects the bank's non-performing loans (NPLs) to gradually improve over the next 12-18 months as Vietnam's GDP growth continues to recover. Furthermore, the organization anticipates that, along with the enactment of several land and real estate laws, Vietnam's real estate sector is expected to recover strongly in 2025. According to S&P and many analysts (based on Q3 2024 results), this will benefit Techcombank due to the bank's business model. S&P notes that the bank's asset quality has been "tested" recently, as despite a significant proportion of outstanding loans in the real estate sector, its real estate-related NPLs have consistently been lower than the overall NPLs. Techcombank has also consistently ranked among the banks with the lowest NPLs and loans requiring attention within the banking system. A key part of S&P's latest assessment is Techcombank's capital structure. The rating agency highly praised the bank's exceptional ability to diversify its funding sources. This allows Techcombank to access diverse funding options with longer maturities and lower funding costs. S&P also believes that Techcombank will "continue to attract diversified, low-cost deposits through innovative savings products and enhanced digital banking experiences. This will help the bank maintain one of the highest current account and savings account (CASA) ratios in the industry and very competitive funding costs." Finally, in its latest announcement, S&P revised its rating in Techcombank's upgrade scenario, stating that it could "upgrade" if the bank's risk-adjusted capital ratio (RAC) improves over the next 12-18 months. This is a significant change from its most recent assessment, which stated "an upgrade is unlikely." This S&P assessment is entirely consistent with Techcombank's announced and implemented strategy to further diversify its credit portfolio. This will significantly alter the asset structure with an increased proportion of assets with lower risk-adjusted weightings. This optimizes the return on total assets adjusted for risk and increases the likelihood of being upgraded by various credit rating agencies in the future.| ASSESSMENT SCORE Issuer's credit rating: BB-/Stable Banking industry rating: b+ Business position: Strong (+1) Capital and income: Moderate Risk position: Appropriate Funding & liquidity: Appropriate and Appropriate Government support: +0 |

Comment (0)