Recently, there have been some rumors in the market about the State Bank's (SBV) expected change in exchange rate management measures.

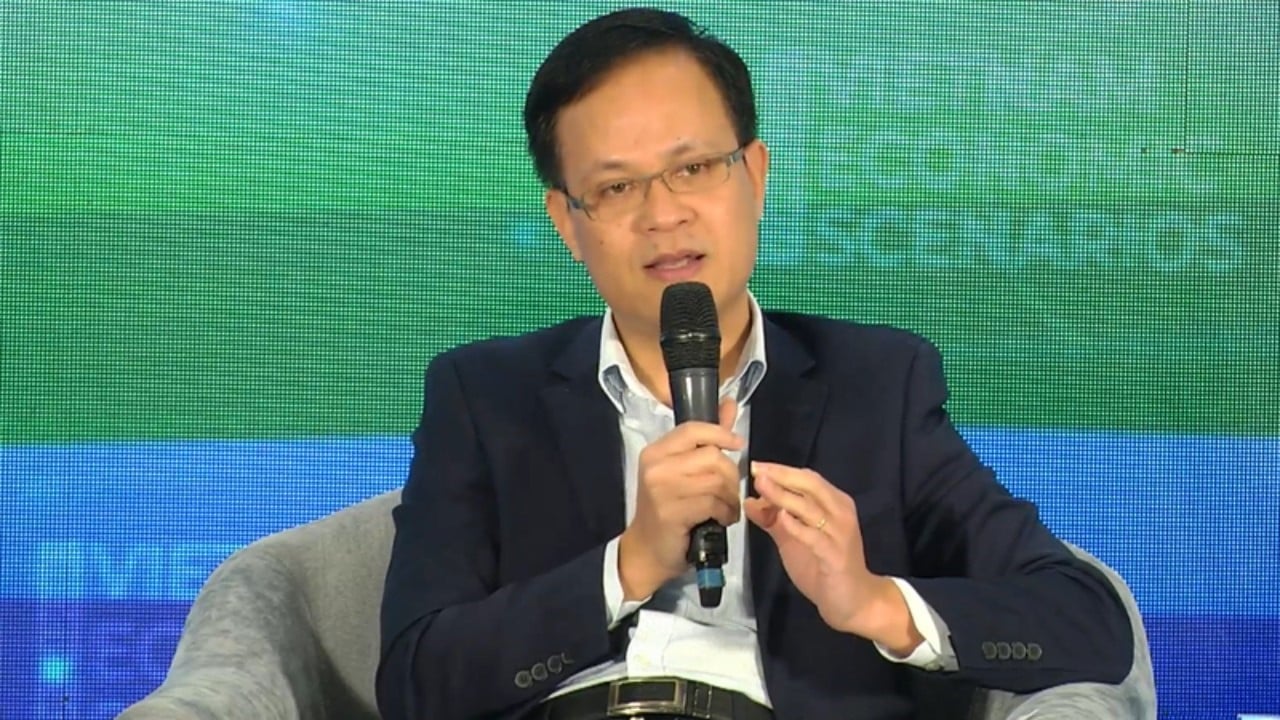

On May 24, Mr. Pham Chi Quang, Director of the Monetary Policy Department of the State Bank of Vietnam, denied the above false rumor.

“Some recent information about changes in the State Bank’s exchange rate management is inaccurate and inconsistent with the Government’s goals of stabilizing the market and the macro economy , creating instability in the market. Therefore, businesses and people need to be cautious,” Mr. Pham Chi Quang affirmed.

Unfounded rumors combined with domestic and international macroeconomic factors have put the exchange rate under a lot of pressure. According to Mr. Pham Chi Quang, the three main reasons leading to the exchange rate tension are:

First of all, inflation remains high in the US, causing the international market to continuously adjust forecasts and postpone the expected date for the US Federal Reserve (Fed) to cut interest rates. The market's changing expectations about the path of monetary policy, the Fed's interest rate cut, along with increasing geopolitical tensions in some territories, caused the international USD to appreciate sharply, at one point the USD index (DXY) increased by 5% compared to the beginning of 2024, creating devaluation pressure on other currencies, including VND.

Second , from the beginning of the year to mid-May 2024, the economy's imports recovered strongly - estimated at 132.23 billion USD, an increase of 19.7 billion USD (up 17.5%) over the same period in 2023, increasing the demand for foreign currency, especially the demand for foreign currency to pay for the import of essential raw materials and fuels for domestic production.

However, importing raw materials at the beginning of the year to serve the economic recovery process will create a premise to promote production and export activities, thereby creating foreign currency revenue in the future, which can relieve some pressure on exchange rates in the coming time.

Third, while the US continues to keep USD interest rates high, VND interest rates are lower than international USD interest rates (causing the interest rate differential between the two currencies to be negative), encouraging economic organizations to buy foreign currency forwards to serve future payments - shifting future foreign currency demand to the present. Meanwhile, customers with foreign currency income have the mentality of delaying the sale of foreign currency to the banking system, making the balance of foreign currency supply and demand less favorable in the short term and putting pressure on the exchange rate.

The Director of the Monetary Policy Department affirmed that all the above difficulties and challenges of the domestic foreign exchange market are only short-term, because in the coming time, with the positive recovery of exports, the market's foreign exchange supply will be supported to increase.

The recent sharp increase in foreign currency futures purchases by businesses is a factor that reduces future foreign currency demand, thereby making the balance of foreign currency supply and demand more likely to improve positively in the future.

At the same time, the international financial community maintains its forecast that the Fed will likely cut interest rates by the end of 2024, thereby reducing devaluation pressure on currencies around the world, including VND.

“With the current central exchange rate management mechanism and +/-5% amplitude, the market exchange rate has enough room for flexible movements,” Mr. Quang affirmed.

Source: https://vietnamnet.vn/ngan-hang-nha-nuoc-bac-tin-don-ve-thay-doi-bien-phap-dieu-hanh-ty-gia-2284241.html

![[Photo] Prime Minister Pham Minh Chinh and Prime Minister of the Kingdom of Thailand Paetongtarn Shinawatra attend the Vietnam-Thailand Business Forum 2025](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/16/1cdfce54d25c48a68ae6fb9204f2171a)

![[Photo] President Luong Cuong receives Prime Minister of the Kingdom of Thailand Paetongtarn Shinawatra](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/16/52c73b27198a4e12bd6a903d1c218846)

Comment (0)