Net withdrawal of 50,000 billion VND

After four consecutive sessions of decline, the VN-Index lost nearly 90 points to below the 1,140-point threshold. Many stocks fell sharply, including real estate and securities stocks. However, the buying pressure that started in today's session helped the VN-Index regain the support level of 1,150 points.

After 3 survey sessions, on September 26, the State Bank of Vietnam (SBV) withdrew an additional VND20,000 billion through the treasury bill channel. The total net withdrawal in 4 sessions reached nearly VND50,000 billion. The interest rate for withdrawing money increased slightly to 0.58%. This is still a record low, lower than the 5-6%/year in late 2022 and early 2023.

However, the volume is not high compared to 25,000-35,000 billion VND/session in December 2022-March 2023. The 28-day withdrawal term this time is also equivalent to the term in mid-November 2022. This shows that liquidity in the banking system is very abundant.

The pumping and pumping activities in the open market are quite normal and do not mean that the State Bank has reversed its monetary policy. This agency is still implementing a loose monetary policy.

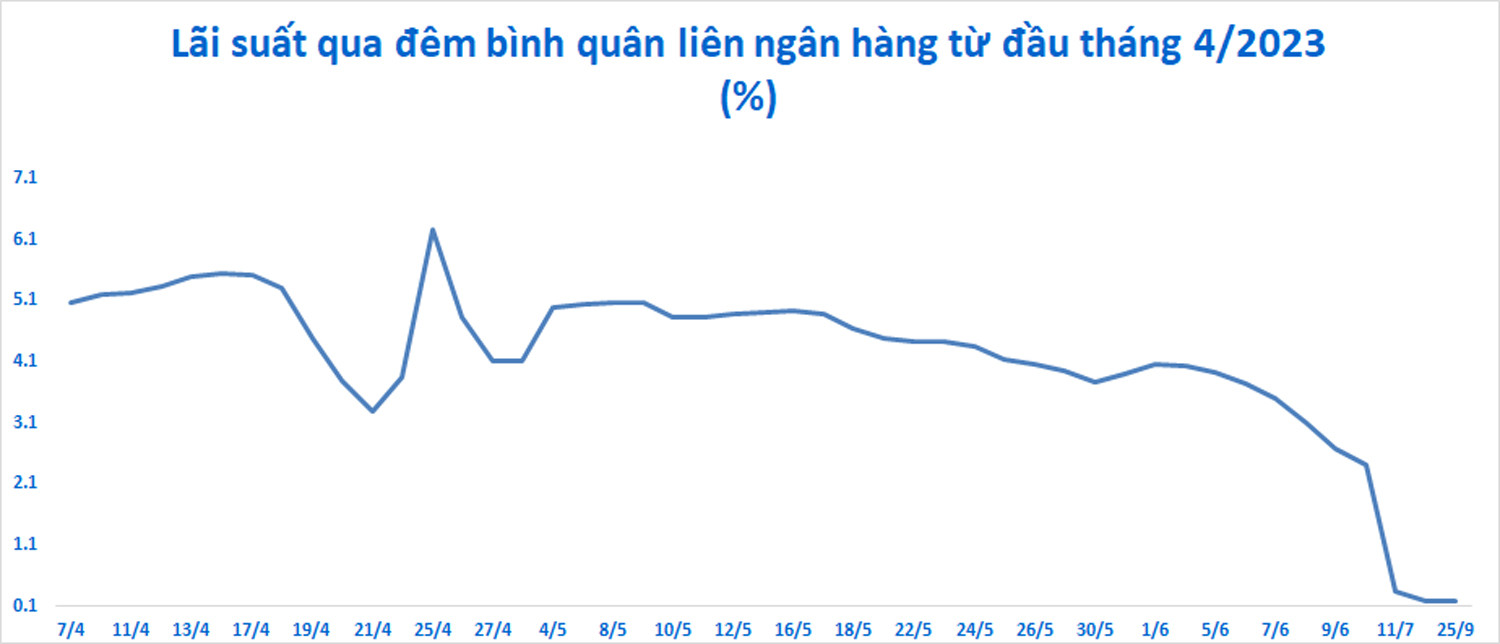

Since March, the State Bank has reduced the operating interest rate by 150-200 points four times. The rediscount rate has been reduced from 4.5% to 3%, the refinancing rate from 6% to 4.5% and the interbank overnight rate from 7% to 5%. The State Bank has also been regularly buying USD.

The return to withdrawing money on the open market took place when the USD/VND exchange rate increased sharply since August, bringing the total increase since the beginning of the year to 3.3%. This is a rapid increase but not as strong and risky as in October 2022.

The USD/VND exchange rate at banks has not surpassed the peak of 24,888 VND/USD recorded in October 2022. The current exchange rate is at 24,540 VND/USD.

Credit growth is very low, only reaching 5.56% as of September 15. Banks are still facing the disease of "excess money".

Overnight lending rates in the interbank market are at record lows, although they have slightly increased from 0.14% (September 21) to 0.17% (September 25). At the end of May 2023, interbank interest rates reached nearly 6.5%/year and a record of 8.44%/year on October 5, 2022.

According to experts, the withdrawal of liquidity from market 2 is to reduce short-term speculative pressure on exchange rates. The withdrawal level is not large, so it will not cause liquidity tension in market 2 and limit the impact on the interest rate level in market 1.

According to MBS Securities, the State Bank's move to absorb VND will push interbank interest rates up slightly and reduce exchange rate pressure in the coming time.

According to the assessment, the State Bank of Vietnam will not withdraw too much money. Investment consultancy FIDT said the withdrawal amount may only be around 100,000 billion VND, double the amount withdrawn in the past 3 sessions.

According to FIDT, the consistent view from the Government and the State Bank is that the deposit and short-term, medium- and long-term lending policies for the economy will have to gradually decrease in the short term. This means that the basic deposit interest rate system of large banks will be very difficult to change. Deposit interest rates are expected to remain at the current level of 3.5% for 3-6 months, 4.5% for 6-12 months and 5.5% for over 12 months. Meanwhile, core inflation has no probability of reaching the target of 4.5%.

According to FIDT, the macro signals are quite positive. Vietnam has the ability to stabilize foreign exchange in the medium and long term. These main foreign exchange flows as of 8 months of this year are still in a positive state. Disbursed FDI decreased slightly, the prospect of new FDI increased. The import-export surplus is at a record high. Remittances may stabilize or decrease slightly following the trend of the global economic slowdown.

The overall foreign exchange position of the State Bank is safe with signs of foreign exchange reserves increasing to 100 billion USD, along with the banking system having a relatively positive USD reserve position.

Are stocks still attractive after the drop?

According to Mirae Asset, the Fed's interest rate hike cycle is coming to an end, the USD is cooling down, thereby reducing pressure on the USD/VND exchange rate. Vietnam will maintain a prudent monetary policy to maintain a balance between stabilizing the exchange rate and reducing lending interest rates.

Stock valuations are more attractive after a sharp decline. Domestic individual investors will continue to play a major role in the market. In August, more than 100,000 new individual accounts were opened.

Mirae Asset believes that growth in most sectors will pick up in the second half of the year thanks to lower lending interest rates, recovery in exports and domestic consumption, accelerated public investment and supportive policies. The long-term outlook is bright as the Vietnam-US relationship is upgraded to a comprehensive strategic partnership.

Dragon Capital also believes in the long-term prospects of stocks. The fund believes that a 5% to 12% decline in volatility during a bull cycle is not uncommon.

However, many domestic securities companies believe that the VN-Index cannot escape the downtrend and the risk of liquidation is always present. The market may still have a strong decline in the near future.

Source

![[Photo] National Assembly Chairman Tran Thanh Man attends the VinFuture 2025 Award Ceremony](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F05%2F1764951162416_2628509768338816493-6995-jpg.webp&w=3840&q=75)

![[Photo] 60th Anniversary of the Founding of the Vietnam Association of Photographic Artists](/_next/image?url=https%3A%2F%2Fvphoto.vietnam.vn%2Fthumb%2F1200x675%2Fvietnam%2Fresource%2FIMAGE%2F2025%2F12%2F05%2F1764935864512_a1-bnd-0841-9740-jpg.webp&w=3840&q=75)

Comment (0)