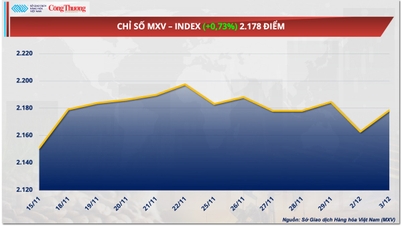

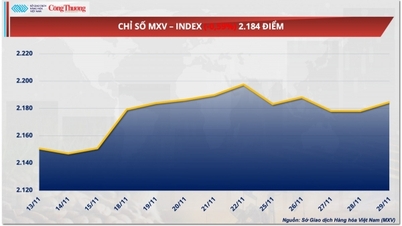

| Oil Market Heads for 7th Weekly Loss on Oversupply Global oil market shifts to domestic supply on Red Sea threat |

The International Energy Agency (IEA) has just reported that global oil demand growth is losing momentum, with demand growth reaching 1.4 million barrels per day (bpd) in January, down from 2.8 million bpd in Q3 2023 to 1.8 million bpd in Q4 2023.

The post-pandemic expansion in demand growth is largely on track, the IEA said. Falling supply is expected to counter slowing demand growth, with supply outside the Organization of the Petroleum Exporting Countries (OPEC) of the United States, Brazil, Guyana and Canada expected to reach 1.6 million barrels per day (bpd) this year, compared with 2.4 million bpd in 2023.

|

| Illustration photo, source Bloomberg |

The best thing for oil bulls, however, is that the oil market is tightening, which could help sustain the ongoing rally in oil prices. The IEA revealed that global observed oil inventories fell by a sharp 60 million barrels in January, with onshore inventories falling to their lowest level since 2016.

In contrast, global inventories rose by 21.6 million barrels in December last year, thanks to surging surface oil prices (+60.7 million barrels) more than offsetting the build in onshore inventories (-39 million barrels). Brent crude rose 7.9% in February to trade at $83.42/bbl while WTI crude rose 9.9% to trade at $79.43/bbl.

Whether the market continues to tighten will largely depend on whether OPEC+ can maintain discipline and gradually lift production cuts. Estimates from various energy agencies on the changes to OPEC’s call are mixed; that is, OPEC crude oil production levels will keep inventories unchanged given changes in non-OPEC supply, oil demand, and OPEC non-crude liquids supply are quite diverse at this point.

With the exception of the IEA, OPEC demand estimates have generally trended upward, reflecting improving overall market fundamentals. These figures indicate how much OPEC can increase production from Q2 onwards without increasing global inventories. The lowest estimates are from the Energy Information Administration (EIA) at 0.6 million barrels per day (mb/d) and the IEA at 0.7 mb/d, while the highest estimates are from Standard Chartered at 1.8 mb/d and the OPEC Secretariat at 2.7 mb/d.

Commodity analysts at Standard Chartered have previously argued that oil fundamentals are in better shape than oil prices suggest, adding that the market is discounting geopolitical risks. StanChart has noted a strong improvement in the oil balance in the current year compared to 2022.

The small global surplus currently seen is due to seasonal weakness in January, according to StanChart, noting that the surplus is much smaller than the 20-year average. StanChart revealed that January inventories have fallen for the first time in just three years since 2004, with the first month of the year averaging an increase of 1.2 million barrels per day (mb/d).

Last year, January recorded a huge surplus of 3.4 million barrels per day, the third-largest surplus for any month in the past two decades. StanChart estimates this year’s January surplus at just 0.3 million barrels per day.

StanChart said it expected Brent crude oil prices to reach at least $90 a barrel to truly reflect market fundamentals. StanChart had predicted that Brent would average $92 a barrel in the first quarter, up 19% from December 31 last year.

Analysts have forecast Brent to hit $98 a barrel in Q3; $109 in 2025 and $128 in 2026 before returning to $115 in 2027. Brent futures on ICE rose $5 a barrel in January, marking the first monthly gain since September last year.

JP Morgan is another bullish oil bull and says its oil outlook continues to predict a tightening market from here with prices rising another $10 by May. JPM’s forecast assumes OPEC+ leaders will roll back the 400,000 bpd cuts from April but has not yet factored in a risk premium from Middle East turmoil.

JPM said crude exports on a 30-day moving average basis are down 1.3 million barrels per day from their October peak. The less optimistic US Energy Information Administration (EIA) forecasts Brent crude prices will average $82.42 in 2024 and $79.48 in 2025, while WTI will average $77.68 a barrel in 2024 and $74.98 in 2025.

Source

![[Photo] Prime Minister Pham Minh Chinh meets with the Policy Advisory Council on Private Economic Development](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/8/387da60b85cc489ab2aed8442fc3b14a)

![[Photo] General Secretary To Lam begins official visit to Russia and attends the 80th Anniversary of Victory over Fascism](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/8/5d2566d7f67d4a1e9b88bc677831ec9d)

![[Photo] National Assembly Chairman Tran Thanh Man chairs the meeting of the Subcommittee on Documents of the First National Assembly Party Congress](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/5/8/72b19a73d94a4affab411fd8c87f4f8d)

Comment (0)