Oil prices suddenly plummeted.

According to MXV, the energy market was in the red during yesterday's trading session. Specifically, the prices of both crude oil and other commodities reversed sharply downwards due to concerns about trade tensions between the US and China.

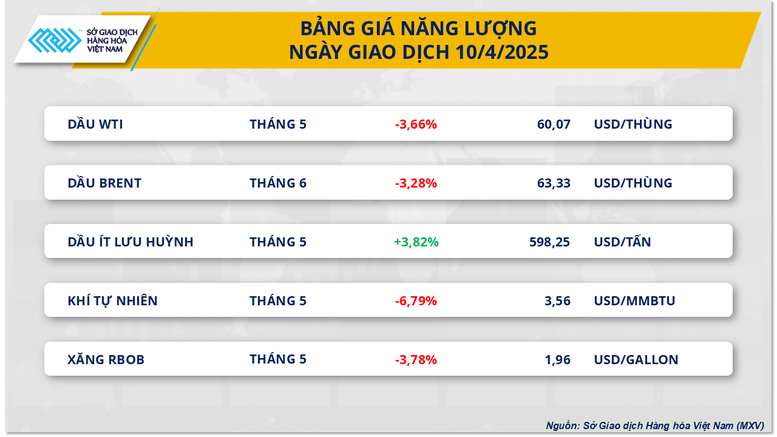

At the close of trading, both Brent and WTI crude oil prices fell by more than 3%. Brent crude recorded a 3.28% decrease, falling to $63.33 per barrel; while WTI crude oil prices returned to near the $60 per barrel mark, currently standing at $60.07 per barrel, a decrease of 3.66%.

In the latest announcement from the White House on April 10, US President Donald Trump raised tariffs on imported goods from China to 145%, including the previous base tariff of 20% and additional tariffs. This move comes after Beijing imposed retaliatory tariffs of 84% on US goods, escalating trade tensions between the world's two largest economies .

Also yesterday, President Trump continued to issue warnings about new sanctions, this time targeting Mexico. In a new post on the social media platform Truth Social, President Trump demanded that Mexico implement the 1944 water agreement between the two countries and transfer 1.3 million acres of water, equivalent to approximately 1.6 billion cubic meters, to the US state of Texas.

Currently, many goods imported into the US from Mexico and Canada are still subject to a 25% tariff due to the fentanyl drug controversy. Canada is also applying a 25% tariff on some imported vehicles from the US as a retaliatory measure. The future of the global economy remains quite uncertain, and concerns about oil demand in the market have not subsided.

Meanwhile, the short-term energy outlook report released yesterday by the US Energy Information Agency (EIA) showed a downward revision of its forecast for global oil demand. The EIA also lowered its forecast for future oil prices due to OPEC+'s production increase plans and concerns about a global economic recession. These factors continue to put significant pressure on the energy market in the coming period.

The entire metals market is covered in green.

At the close of trading yesterday, the metals market witnessed a strong rebound across all 10 commodities. According to MXV, the main reasons supporting this upward trend were concerns about trade tensions, supply shortages, and the US easing monetary tightening.

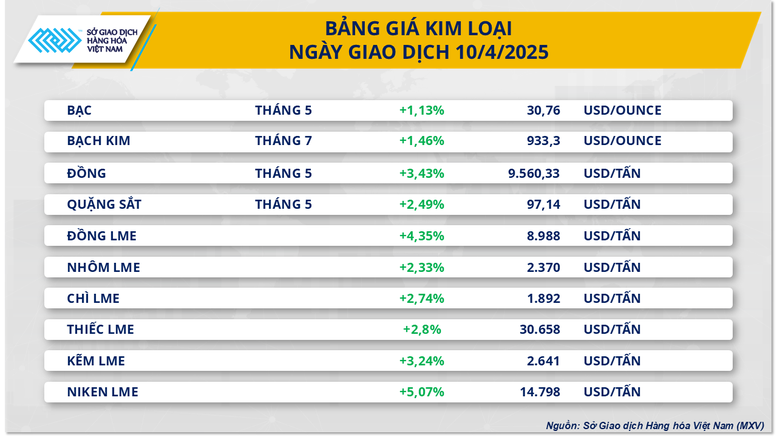

At the close of trading, silver prices rose 1.13% to $30.76 per ounce. Meanwhile, platinum also increased 1.46%, to $933.3 per ounce.

Precious metals continued to receive support as global trade tensions escalated following news that China raised retaliatory tariffs on goods imported from the US.

In addition, according to the minutes of the Federal Reserve's March meeting, released yesterday (April 9), policymakers agreed to slow the pace of quantitative tightening (QT). This means the Fed will loosen monetary policy, thereby helping to maintain ample liquidity in the banking system and encouraging money flows into safe-haven assets such as precious metals.

In other developments, the European Union (EU) and China are holding talks to establish a price floor for electric vehicles (EVs), replacing the 45.3% tariff that the EU has imposed since October 2024. This move is seen as an attempt to ease trade tensions between the two sides, amid increasing pressure from the US on both the EU and China.

The promotion of electric vehicle consumption in Europe could reduce demand for platinum – a key metal used in catalytic converters for gasoline and diesel vehicles. This has helped to curb the rise in platinum prices on the international market. Meanwhile, negotiations between the EU and China are not only aimed at reducing tariffs but also at maintaining stability in global supply chains, creating a more favorable environment for the development of the electric vehicle industry.

For base metals, COMEX copper prices surged 3.43%, to $9,560 per ton. Meanwhile, iron ore jumped 2.49% to $97.14 per ton.

Copper prices received support yesterday due to concerns about shrinking supply. According to data released Thursday by Chile's National Copper Commission (Cochilco), copper production by Chile's state-owned mining company Codelco fell 6% year-on-year in February to 98,100 tonnes. Codelco is currently the world's largest copper producer, but has struggled in recent years to improve its declining output.

Meanwhile, iron ore prices benefited from expectations that Beijing would implement further economic stimulus packages to counter escalating trade tensions. Chinese Premier Li Qiang emphasized that the country needed to implement proactive macroeconomic policies and accelerate their deployment, thereby contributing to bolstering market sentiment.

Source: https://baochinhphu.vn/mxv-index-noi-dai-da-phuc-hoi-sang-phien-thu-hai-102250411085231086.htm

Comment (0)