Chinese President Xi Jinping's efforts to change the country's growth model are facing unprecedented obstacles.

For decades, China accelerated its economy by investing in factories, skyscrapers, and roads. This model generated phenomenal growth, transforming China into the world's second-largest economy and the global manufacturing hub.

But now, they are facing unprecedented obstacles. The $18 trillion economy is slowing down. Consumers are hesitant to spend. Exports are declining. Prices are falling, and more than 20% of young people are unemployed. Country Garden – the country's largest privately owned real estate firm with 3,000 projects – is at risk of default. Zhongzhi Enterprise Group – one of China's largest shadow banks – is also facing customer backlash for delayed payments.

Much of this challenge stems from the efforts of Chinese leaders to transform their growth model. They are unwilling to rely heavily on debt like previous governments . This is evident in the fact that, even when the real estate crisis worsened, China did not implement drastic measures.

This has led many foreign banks, such as JPMorgan Chase, Barclays, and Morgan Stanley, to lower their growth forecasts for China this year, below the government's 5% target. Foreign investors are also withdrawing money, prompting the People's Bank of China (PBOC) to seek ways to stem the yuan's decline.

![[A highway project stalled in Guizhou (China). Photo: Bloomberg]](https://vstatic.vietnam.vn/vietnam/resource/IMAGE/2025/1/19/3ba509fed45c4bd9b42e872c18f67011)

A highway project is stalled in Guizhou, China. Photo: Bloomberg

While the U.S. is spending trillions of dollars supporting households and building infrastructure to stimulate the economy, Chinese President Xi Jinping does not want growth to depend on speculative construction and further borrowing. Experts believe that the contrasting policies between the world's two largest economies are changing global investment flows. It could also slow down, or even prevent, China from overtaking the U.S.

The biggest risk for Chinese officials is that their firm stance against aggressive stimulus could erode confidence in the 1.4 billion-person market. "China is experiencing a downturn in expectations. When people forecast slower growth, it actually slows," Bert Hofman, former World Bank country director for China, commented on Bloomberg.

In a worst-case scenario, China could fall into a state of stagnation similar to Japan's in recent decades. This warning comes after July CPI data showed China entering deflation. Falling prices are a sign of weak demand and slowing future growth. This is due to families delaying purchases, declining corporate profits, and rising real borrowing costs.

SCMP notes that a growing lack of confidence in China's economic growth is emerging as the post-Covid-19 recovery loses momentum. In the second quarter, the world's second-largest economy's GDP grew by 6.3% year-on-year. This rate was higher than in the first quarter (4.5%), but lower than forecasts from many organizations.

Another indicator of economic confidence is the value of the yuan. Since the beginning of the year, the currency has depreciated by 6% against the USD. The yuan's decline is due to China's monetary policy being the opposite of that of the US, investor concerns about weak growth in China, and the risk of default in the real estate sector.

In recent weeks, observers have noted that Chinese authorities have sought to prevent the yuan from depreciating further. The PBOC sets a daily reference rate to help the yuan strengthen. State-owned banks have also been continuously selling US dollars.

Economists believe that China is entering a period of much slower growth, due to an unfavorable demographic structure and a desire for independence from the US and its allies, which threatens foreign trade and investment. This is not just a temporary slowdown; the Chinese economy could enter a prolonged period of stagnation.

"We are witnessing a shift that could lead to the most dramatic turning point in economic history," Adam Tooze, a professor specializing in economic crises at Columbia University, commented in the Wall Street Journal.

In a period of volatile markets, a downturn in China would trigger a global sell-off of risky assets. This happened in 2015, when China's devaluation of the yuan and the subsequent plunge in its stock market forced the Federal Reserve to halt interest rate hikes. The current situation hasn't reached that point yet. But if things continue to worsen, the Fed may have to cut interest rates sooner than expected.

Chinese leaders are not sitting idly by either. Following last month's meeting, they put forward several proposals such as increasing infrastructure spending, providing liquidity support for real estate companies, and easing regulations on home purchases. Last week, China also unexpectedly lowered interest rates.

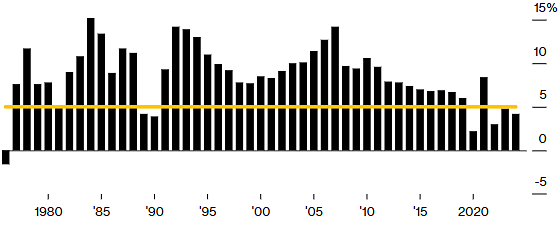

China's annual GDP growth rate since 1976. Graph: Bloomberg

A post last week in the Global Times also suggested that what the Chinese economy needs most right now is confidence. The interest rate cut announcement shows the government's determination to support the economy.

The Global Times observes that China is facing numerous challenges, such as a weakening global economic recovery and unbalanced domestic growth. New issues that emerged in the first half of this year have further complicated the macroeconomic management of the country's officials. However, they argue that "the Chinese economy is gradually recovering" and that the country "has sufficient tools to maintain stable growth," for example, by lowering interest rates.

In fact, several components of the Chinese economy are still booming, such as electric vehicles, solar power, wind power, and batteries. In these sectors, investment and exports are growing at double-digit rates. This is the kind of green, high-tech growth that Chinese leaders aspire to. The country is also issuing bonds for high-speed rail and renewable energy projects on a world-leading scale. They are also lowering lending rates for businesses and providing generous subsidies for electric vehicle buyers.

Tourism and restaurants are also booming compared to last year's lockdown period. Starbucks recorded a 46% increase in revenue in China last quarter. Domestic flights are now 15% busier than before the pandemic. Travelers are also complaining that budget hotels are raising prices due to the surge in demand. These activities are creating jobs, helping to alleviate officials' concerns about unemployment rates.

However, the problem is that these new growth engines are not enough to offset the massive slump in the real estate market. Beijing estimates that the "new economy" (comprising green manufacturing and high-tech sectors) grew by 6.5% in the first half of this year and contributed about 17% of GDP. Conversely, spending on construction fell by 8% in the first half of the year. This sector contributes 20% of GDP, both directly and indirectly.

The Chinese real estate market has been in turmoil since late 2020, when the government introduced its "three red lines" policy to curb the debt bubble and slow the rise in house prices. However, it also deprived real estate companies of key sources of capital. Real estate giant China Evergrande Group defaulted on its debt at the end of 2021 and filed for bankruptcy protection in the US last week. Recently, another major Chinese real estate company, Country Garden, also warned of "uncertainty" regarding its ability to repay its bonds.

Real estate sales in China are currently less than 50% of their 2020 peak. Not only are real estate and related industries (construction, steel, cement, glass) affected, but household confidence has also plummeted. This is because real estate accounts for approximately 70% of Chinese household assets, according to Citigroup data. Properties also represent 40% of assets currently mortgaged at banks.

Falling housing prices make families feel poorer, leading them to tighten their spending, further constricting growth. As businesses lower profit expectations, reduce investment, and cut back on hiring, the ripple effect will be even greater.

Some experts have urged Beijing to break this vicious cycle with confidence-building measures. PBOC advisor Cai Fang recently urged the government to provide direct support to consumers. Many other economists also suggest the government could borrow several trillion yuan (hundreds of billions of US dollars) to stimulate consumption.

However, Beijing did not accept these proposals. "The best way to support consumption is through supporting employment. That is, supporting the business sector through tax cuts," said Wang Tao, an economist at UBS. Xi Jinping also frequently reminded Chinese officials that they should not sacrifice the environment, national security, and risk mitigation capabilities for growth.

However, observers believe that the possibility of China taking drastic action cannot be ruled out. For example, last year, the country abruptly abandoned its Zero Covid policy after three years of implementation.

Zhu Ning, a professor at the Shanghai Institute of Advanced Finance and currently an advisor to the Chinese government, has observed a recent shift in officials' views on the real estate sector. Zhu predicts that China will introduce even stronger support measures.

"The question is whether they are willing to sacrifice the fiscal deficit. Currently, they are hesitant. But economic realities may cause leaders to change their minds," he concluded.

Ha Thu (according to Bloomberg, WSJ, Global Times)

Source link

![[Image] Close-up view of the interchange connecting the two expressways and Long Thanh Airport.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779703378210_ndo_br_z7863716673926-224453a31600126cce10622af6290afd-4549-jpg.webp)

![[Image] Hanoi's urban life under the challenge of a "scorching hot" environment](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2026/05/25/1779706979265_nang-nong-t5-2026-minh-duy-7-4636-jpg.webp)

Comment (0)