Following a slow recovery in the third quarter, Mr. Dinh Quang Hinh - Head of Macroeconomics and Market Strategy at VNDIRECT Securities - expects Vietnam's economic recovery to accelerate further in the fourth quarter.

The main drivers of support will come from expansionary fiscal policy. Lower lending rates are improving private investment and domestic consumption. The manufacturing recovery is accelerating thanks to a resurgence in export orders amid declining inventories and easing inflationary pressures in developed markets. Finally, there is the low base of the same period in 2022.

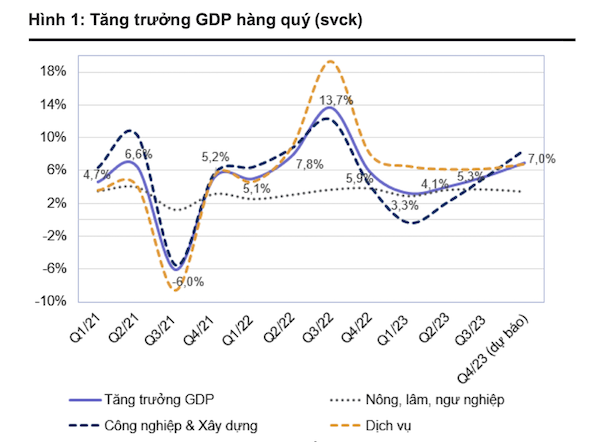

"We forecast Vietnam's GDP to grow by 7.0% year-on-year in Q4 2023, a significant improvement from the 5.3% growth in the previous quarter. The industrial and construction sectors could improve their growth rate to 8.2-8.7% year-on-year in Q3 2023 thanks to improved production, exports, and strong public investment disbursement. I expect the service sector to grow by 6.5-7.0% year-on-year, while the agriculture, forestry, and fisheries sector is projected to grow by 3.4-3.6% year-on-year," Mr. Hinh predicted.

Despite expectations of a clearer recovery in the fourth quarter, VNDIRECT experts have lowered their 2023 GDP growth forecast in the base scenario to 5.0% from the previous forecast of 5.5%. This is mainly due to lower-than-expected results in the first nine months of 2023.

Meanwhile, experts from KBSV Securities expect positive signs in the macroeconomic environment to return in the last quarter of 2023. The main drivers will come from the recovery of export activities leading to industrial production growth; the government accelerating the disbursement of investment capital and FDI; and the recovery of domestic consumption thanks to demand-stimulating policies.

Conversely, renewed inflationary and exchange rate pressures are forcing the State Bank of Vietnam to be more cautious in its monetary policy. In addition, the domestic real estate market still shows no signs of recovery, posing risk factors that are hindering GDP growth.

"The lag in policy implementation remains a positive macroeconomic factor in the coming period. However, concerns about exchange rate pressure and inflation could cause the macroeconomic environment to fluctuate in an unfavorable direction in Q4 2023 and the first half of 2024," KBSV commented.

Source

Comment (0)